Canadian Dental Plans: Your 2026 Coverage Guide

June 7, 2026

Canadian Dental Plans: Your 2026 Coverage Guide

TL;DR:

- Canadian dental plans, including the public CDCP and private insurance, help Canadians manage dental costs by covering essential services and filling coverage gaps. Eligibility for the CDCP depends on income, private insurance status, and residency, with tiered benefits based on net income, but it excludes orthodontics and cosmetic procedures unless medically necessary. To maximize coverage, families should understand plan limitations, renew on time, and consider private insurance for orthodontics and implants, often paying between $75 and $150 monthly per adult.

Canadian dental plans are insurance programs that reduce the out-of-pocket cost of dental care for eligible individuals and families in Canada. The federal government’s Canadian Dental Care Plan (CDCP), administered by Sun Life, now covers over 6.5 million Canadians as of April 2026, with members saving an average of $900 per year on dental expenses. That enrollment figure signals how large the unmet need for affordable dental care was before the CDCP expanded. Private dental insurance from providers like Manulife, Sun Life, and Great-West Life fills the gaps the public plan does not cover, including orthodontics and cosmetic procedures. Understanding both systems is the fastest way to protect your family’s oral health without overpaying.

How does the Canadian Dental Care Plan work and who qualifies?

The CDCP is the federal public program designed for Canadians who have no access to private dental insurance. It is not a universal benefit. To qualify, you must meet four conditions: no existing private dental coverage, an adjusted family net income under $90,000, Canadian residency for tax purposes, and a filed tax return for the previous year.

That income threshold trips up more applicants than you might expect. Adjusted family net income is not your gross salary. It is your net income after deductions like RRSP contributions and childcare expenses, which means some families who assume they earn too much actually qualify once deductions are applied.

Once approved, coverage is tiered by income:

- Full coverage (100%): Adjusted family net income under $70,000

- Partial coverage (60%): Income between $70,000 and $79,999

- Partial coverage (40%): Income between $80,000 and $89,999

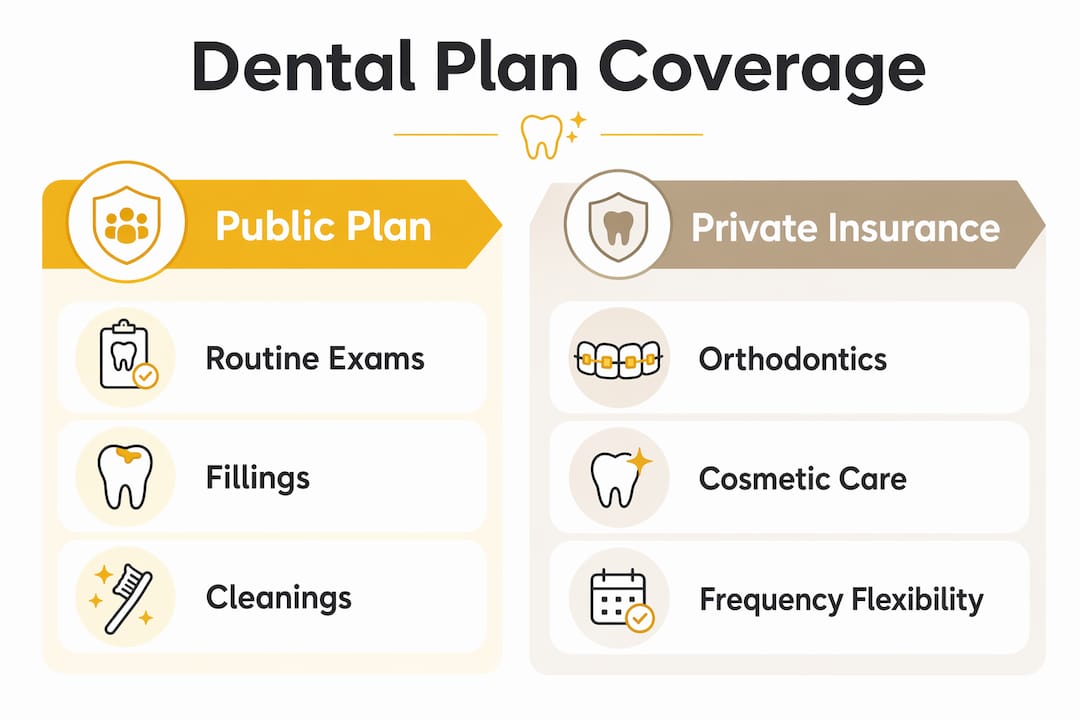

The CDCP covers a broad range of essential dental services including exams, cleanings, fillings, extractions, root canals, and dentures. Cosmetic procedures, implants, and most orthodontic treatments are excluded unless a dentist certifies medical necessity.

Renewal for the 2026 to 2027 benefit year is time-sensitive. The renewal deadline was June 1, with re-enrollment opening June 2 for those who missed the window. Missing that date creates a gap in coverage, meaning any dental work done during the lapse is entirely out of pocket. Mark it in your calendar the same way you would a tax deadline.

Nearly all active oral health providers in Canada, including dentists, hygienists, and denturists, now accept CDCP patients. That near-universal participation removes one of the biggest practical barriers to using the plan.

What services do Canadian dental plans cover and what are the limitations?

The gap between what the CDCP covers and what private dental insurance covers is wider than most people realize. Here is a direct comparison:

| Service | CDCP (public) | Private dental insurance |

|---|---|---|

| Routine exams and cleanings | Covered | Covered |

| Fillings and extractions | Covered | Covered |

| Root canals | Covered | Covered (limits vary) |

| Dentures | Covered | Covered (limits vary) |

| Orthodontics (braces, Invisalign) | Excluded (unless medically necessary) | Often covered up to a lifetime max |

| Dental implants | Excluded | Sometimes covered, plan-dependent |

| Cosmetic procedures (whitening, veneers) | Excluded | Excluded by most plans |

| Pre-authorization requirements | Required for some procedures | Required for major work |

The CDCP also applies frequency caps. For example, routine cleanings may only be covered once every nine months rather than the twice-yearly schedule many dentists recommend. Pre-authorization is required for higher-cost procedures like dentures and some restorative work, and providers must submit those requests before treatment begins, not after.

Private dental insurance fills the orthodontic gap most directly. If your child needs braces or Invisalign, the CDCP will not help unless a physician documents a medical necessity. Understanding braces insurance coverage before you book a consultation saves you from an unpleasant billing surprise. Similarly, parents researching Invisalign insurance options will find that private plans vary significantly in their lifetime orthodontic maximums, typically ranging from $1,500 to $3,000 per person.

Pro Tip: Ask your dental office to run a pre-treatment estimate through your plan before any major procedure. This gives you the exact covered amount and your expected co-payment before you commit to treatment.

The CDCP is designed as a program for those without private dental insurance, not a full replacement for it. Families with complex dental needs, particularly those with teenagers who may need orthodontic treatment, will almost always benefit from layering private coverage on top of any public benefits they receive.

How much do Canadian dental plans cost and how to manage affordability?

The CDCP costs nothing in premiums for eligible Canadians. Your only potential expense is the co-payment portion based on your income tier, and even that is zero for families earning under $70,000.

Private dental insurance is a different calculation. Adult premiums in Canada typically run between $75 and $150 per month, depending on age, province, and coverage level. A family plan covering two adults and two children can easily reach $250 to $350 per month. That cost is real, but so is the protection it provides against a $4,000 orthodontic bill or an unexpected crown.

Here are four strategies to manage dental costs effectively:

- Prioritize preventive care. Cleanings and exams covered by your plan cost far less than the fillings and root canals that result from skipped appointments. Preventive visits are the highest-return use of any dental benefit.

- Understand your annual maximum. Most private plans cap total annual benefits between $1,000 and $2,500. Scheduling major work strategically across two calendar years can double your effective coverage.

- Confirm coverage before every appointment. Plans change at renewal, and so do covered codes. A quick call to your insurer before a procedure prevents billing disputes later.

- Check employer group plans first. Group dental benefits through an employer are almost always cheaper per dollar of coverage than individual private plans. If your employer offers a plan, enroll before shopping individually.

Pro Tip: When comparing private dental plans, look at the waiting period for major services. Some plans require 3 to 6 months of enrollment before covering crowns or orthodontics. If your child’s orthodontic treatment is imminent, a plan with no waiting period is worth paying a slightly higher premium.

The CDCP’s $900 average annual savings figure is meaningful context here. For a family earning $68,000 with two kids, that savings effectively offsets a significant portion of what a private supplemental plan would cost, making the combination of public plus private coverage the most financially sound approach for many Canadian families.

How to apply for and maintain your dental plan coverage

Applying for the CDCP is straightforward, but the sequence matters. Follow these steps to avoid the most common pitfalls:

- File your taxes first. The CDCP uses your most recent Notice of Assessment to verify income. Applications submitted before your tax return is processed will be delayed.

- Apply online or by phone. Use your My Service Canada Account to apply online, or call 1-833-537-2635. Phone applications are available for those without online access.

- Gather your documents. You will need your Social Insurance Number, your Notice of Assessment, and confirmation that you have no private dental insurance. If you recently lost employer coverage, have the cancellation date ready.

- Wait for your welcome letter. Sun Life sends a welcome package with your member ID and coverage start date. Do not book any dental appointments until you have this letter and your coverage is confirmed active.

- Renew annually. Coverage does not renew automatically. The 2026 renewal window opened April 15 and closed June 1. Set a recurring reminder for mid-April each year.

- Notify Service Canada of changes. If you gain private dental insurance, your income changes significantly, or your family composition changes, you must report it. Failing to do so can result in repayment of benefits received while ineligible.

One critical point that catches many new enrollees off guard: Sun Life reimburses providers directly, not patients. If you pay your dentist in full out of pocket, you cannot submit for reimbursement later. Coverage is not retroactive, and appointments booked before your official coverage start date are entirely your financial responsibility. This is the single most expensive mistake CDCP enrollees make.

For private dental insurance, the application process varies by provider. Manulife, Sun Life’s individual division, and Canada Life all offer online applications with same-day approval for basic plans. For families with teenagers considering orthodontic treatment, reviewing braces coverage in Langley and similar regional guides helps you understand what local providers actually accept before you commit to a plan.

Key takeaways

The most effective approach to Canadian dental plans is combining CDCP eligibility with targeted private insurance to cover orthodontics, implants, and services the public plan excludes.

| Point | Details |

|---|---|

| CDCP eligibility criteria | No private insurance, income under $90,000, filed taxes, Canadian residency required. |

| Annual renewal is mandatory | Miss the June 1 deadline and you face a gap in coverage with no retroactive protection. |

| Private insurance fills key gaps | Orthodontics, implants, and cosmetic work require private coverage; CDCP excludes them. |

| Provider reimbursement model | Sun Life pays providers directly; patients who pay out of pocket cannot claim it back. |

| Cost of private plans | Adult premiums run $75 to $150 per month; family plans typically reach $250 to $350 monthly. |

What I’ve learned from watching families navigate dental coverage

Most families I’ve seen struggle with dental plans make the same mistake: they treat the CDCP as a complete solution and skip private coverage entirely. That works fine until a teenager needs orthodontic treatment or an adult needs an implant. Then the bill arrives and the shock is real.

The CDCP is genuinely valuable. An average savings of $900 per year is not a rounding error for a family on a tight budget. But the program was built to address a baseline access problem, not to replicate the breadth of a good employer group plan. Treating it as a floor rather than a ceiling is the right mental model.

The renewal deadline issue is the one I find most frustrating to watch. People enroll, forget to renew, and then show up to a dental appointment in July with lapsed coverage. The fix is trivially simple: set a phone reminder for April 15 every year. That one habit prevents a problem that costs real money.

My honest advice is to spend 30 minutes comparing your CDCP coverage against one or two private plan options before your next renewal. The math usually makes the right answer obvious. And if orthodontic care is on the horizon for anyone in your household, have that conversation with your dental provider now, not after treatment starts.

— Juiced

How Glow Orthodontics supports your family’s dental care journey

Orthodontic treatment sits outside what most Canadian dental plans cover by default, which is exactly where Glow Orthodontics comes in. The team at Gloworthodontics specializes in Invisalign and orthodontic treatments for families in the Langley, British Columbia area, and they work with patients to understand what their private insurance covers before treatment begins. If you have a teenager approaching the age where braces or Invisalign makes sense, the orthodontic care guide for teens is a practical starting point for understanding timelines, costs, and what to ask your insurer. Book a consultation with Gloworthodontics to get a clear picture of your treatment options and how your dental plan applies.

FAQ

What is the Canadian Dental Care Plan?

The Canadian Dental Care Plan (CDCP) is a federal public program that provides dental coverage to eligible Canadians who have no private dental insurance and meet income and residency requirements. It covers essential services like cleanings, fillings, and root canals, administered by Sun Life.

Who qualifies for the CDCP in 2026?

You qualify if you have no private dental insurance, your adjusted family net income is under $90,000, you are a Canadian resident for tax purposes, and you have filed your previous year’s tax return. Coverage levels are tiered based on income.

Does the CDCP cover braces or Invisalign?

The CDCP excludes most orthodontic treatments, including braces and Invisalign, unless a dentist certifies medical necessity. Families seeking orthodontic coverage typically need private dental insurance, which often includes a lifetime orthodontic maximum between $1,500 and $3,000.

How much does private dental insurance cost in Canada?

Private dental insurance for an adult in Canada typically costs between $75 and $150 per month, depending on age, province, and the level of coverage selected. Family plans covering two adults and children generally run $250 to $350 per month.

Can I get reimbursed if I pay my dentist out of pocket under the CDCP?

No. Sun Life reimburses oral health providers directly under the CDCP. If you pay your dentist in full before your coverage is active, or before the provider submits a claim, you cannot receive retroactive reimbursement for that expense.