Financing Orthodontic Treatment: A Smart Family Guide

May 20, 2026

Financing Orthodontic Treatment: A Smart Family Guide

TL;DR:

- Orthodontic treatment costs vary widely, but flexible financing options, including in-house plans, third-party loans, and FSA or insurance benefits, can make payments easier. Early evaluation and strategic payment planning, such as negotiating discounts and combining benefits, reduce overall expenses and treatment complexity. Proactive communication with providers ensures ongoing treatment even if financial difficulties arise during the process.

Orthodontic treatment costs catch most families off guard. Traditional braces or Invisalign can run anywhere from $3,000 to $10,000 depending on complexity, and many people assume the full amount is due before treatment even begins. That assumption keeps a lot of people from getting care they need. Financing orthodontic treatment is more flexible than most providers let on, and knowing your options before you sit down for a consultation gives you real leverage. This guide covers every major payment strategy, how to combine them, and what to watch out for so you can say yes to treatment without wrecking your budget.

Table of Contents

- Key takeaways

- Financing orthodontic treatment: what it actually costs

- Common ways to finance orthodontics

- Strategies to reduce your out-of-pocket cost

- Why early evaluation changes the cost equation

- What to do if payments become difficult mid-treatment

- My honest take on financing orthodontic care

- Flexible financing at Glow Orthodontics

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Financing options are varied | In-house plans, third-party lenders, HSA/FSA funds, and insurance can all be combined to reduce costs. |

| Upfront discounts exist | Paying in full can save 5 to 10% off total treatment cost, often hundreds of dollars. |

| Early evaluation saves money | A child’s orthodontic check-up by age seven can shorten treatment and lower the overall financial commitment. |

| Deferred interest is a trap | Some 0% financing offers trigger retroactive interest from the start date if any payment is missed. |

| Negotiation is expected | Orthodontic offices routinely adjust down payments and payment schedules. You just have to ask. |

Financing orthodontic treatment: what it actually costs

Before you can plan payments, you need a clear picture of the numbers. Treatment costs vary significantly based on the type of appliance, the complexity of your case, and where you live.

| Treatment type | Typical cost range |

|---|---|

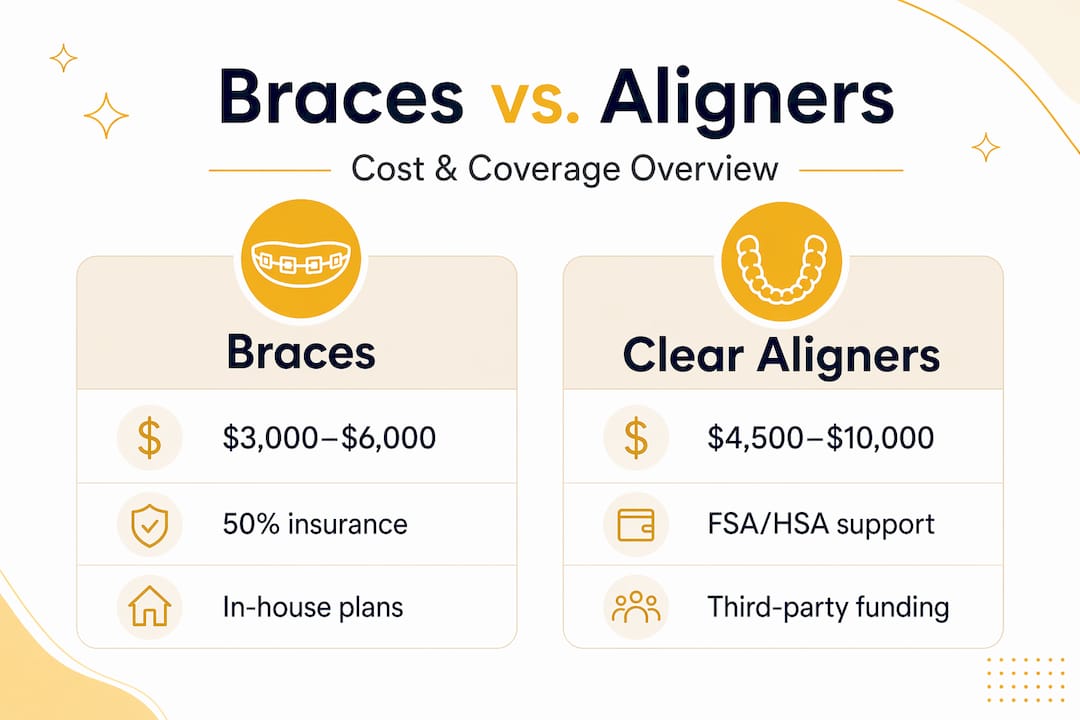

| Traditional metal braces | $3,000 to $6,000 |

| Ceramic (clear) braces | $4,000 to $8,000 |

| Invisalign or clear aligners | $4,500 to $10,000 |

| Retainers (post-treatment) | $150 to $600 |

A few factors push costs toward the higher end of those ranges:

- Severity of misalignment: More complex bite issues require longer treatment and more frequent adjustments.

- Treatment length: Cases spanning 24 months or more cost more than shorter 12-month corrections.

- Geographic location: Urban areas in Canada and the U.S. tend to have higher overhead costs, which gets passed along to patients.

- Inclusions in the fee: Most quality providers bundle consultations, all adjustment appointments, and initial retainers into one treatment fee. Always ask what is and is not included before comparing quotes.

One common misconception is that a lower quoted price means a better deal. A practice that charges $4,500 but includes all adjustments and a retainer may cost less overall than a practice quoting $3,800 with fees billed separately. Breaking down exactly what each quote covers is one of the most practical steps you can take during consultations.

If you are comparing treatment options, understanding the cost differences between clear aligners and traditional braces can help you make a financially informed choice from the start.

Common ways to finance orthodontics

Most orthodontic practices offer several ways to spread out costs, and the best strategy often involves layering more than one option.

In-house payment plans

Many orthodontists offer their own in-house financing plans with 0% interest for 12 to 24 months and no credit check required. A typical arrangement requires a down payment of 20 to 30% of the total cost, with monthly payments starting once treatment begins. These plans are straightforward and do not carry the risk of retroactive interest penalties that some third-party products carry.

The downside is that the monthly payments are fixed to the treatment timeline, and the practice may not offer enough flexibility if your financial situation changes mid-treatment.

Third-party healthcare financing

Companies like CareCredit offer 0% promotional financing with terms extending up to 60 months for qualifying applicants. They require a credit check and approval, and the longer terms can make large balances feel manageable.

The critical warning: these products often include deferred interest clauses. If you miss even one payment or carry a balance past the promotional period, interest is calculated from the original transaction date, not from when the promotional period ended. That can turn a $6,000 treatment into a significantly larger debt quickly. Always read the financing agreement in full before signing.

HSA and FSA accounts

Health Savings Accounts and Flexible Spending Accounts let you pay for orthodontic care with pre-tax dollars, which can reduce costs by 20 to 30% depending on your tax bracket. As of 2026, individuals can contribute up to $3,200 annually to an FSA. That is a meaningful amount that can cover a large portion of a down payment or several months of monthly payments.

For parents wondering about Invisalign specifically, FSA funds generally qualify. You can find more detail on FSA coverage for Invisalign on the Gloworthodontics resource library.

Dental insurance

Dental insurance covers roughly 50% of orthodontic treatment up to a lifetime maximum that typically ranges from $1,500 to $3,000. Children are more commonly covered than adults, and adult plans sometimes require proof of medical necessity. Understanding your specific plan’s orthodontic rider before starting treatment is worth the phone call to your insurer.

For a thorough breakdown of what insurance typically covers in the Langley area, the braces insurance guide at Gloworthodontics is a good starting point.

Pro Tip: Ask your orthodontic office to bill your insurance directly and then set up a payment plan only for the remaining balance. This keeps your monthly obligation as small as possible from the beginning.

Strategies to reduce your out-of-pocket cost

Understanding the options is step one. Putting them together smartly is where real savings happen.

-

Layer your HSA or FSA with a monthly payment plan. Use tax-advantaged funds to cover the down payment, then use an in-house monthly payment plan for the remaining balance. Combining these methods reduces both your upfront cash burden and your overall taxable cost.

-

Ask about upfront payment discounts. Many practices offer 5 to 10% off for patients who pay in full at the start of treatment. A significant number of patients miss this discount simply because they do not know to ask. If you have the cash flow or can use HSA funds to cover most of the treatment, it is worth calculating the savings.

-

Negotiate the down payment. Orthodontic offices, especially those building long-term relationships with families, are often willing to adjust the required down payment or stretch out the payment schedule. You are more likely to get flexibility if you are upfront about your budget during the initial consultation rather than after treatment begins.

-

Check for family discounts. If two or more family members are in treatment at the same time, many practices offer family discounts of 10 to 20% on subsequent cases. Ask specifically whether this applies if treatments overlap even partially.

-

Look into dental school clinics and nonprofit programs. Accredited dental school orthodontic programs offer treatment at significantly reduced rates, performed by supervised graduate students. This is not for everyone, but for families with budget constraints it is a legitimate option worth researching locally.

-

Watch for seasonal promotions. Many practices run new-patient specials or discounted consultation periods during back-to-school season in late summer. Timing your consultation strategically could translate to real savings.

Pro Tip: Before your consultation, call your insurance provider to confirm your orthodontic lifetime maximum and whether it has been used. Walk into the consultation knowing that number. It changes the entire conversation about financing.

Why early evaluation changes the cost equation

Orthodontic treatment for children often costs less and takes less time when problems are caught early. The American Association of Orthodontists recommends that children receive an initial orthodontic evaluation by age seven. That is earlier than most parents expect.

Why seven? At that age, a child has a mix of baby and permanent teeth, which gives an orthodontist a clear view of how adult teeth are coming in and whether the jaw is developing properly. Early intervention can prevent more complex issues from forming, which directly reduces the scope and cost of treatment later.

Signs that a child may benefit from an early evaluation include:

- Difficulty chewing or biting

- Mouth breathing or snoring

- Early or late loss of baby teeth

- Crowding, shifting, or misplaced teeth

- Jaw that clicks or appears off-center

Early orthodontic assessments enable treatment during growth phases, when correction is less invasive and shorter in duration. A proactive evaluation often costs nothing beyond your child’s regular dental visit and could save thousands down the line.

What to do if payments become difficult mid-treatment

Life changes. Job losses, unexpected expenses, or a change in insurance coverage can all disrupt a payment plan mid-treatment. The worst move is to go silent.

If orthodontic payments stop, treatment may be paused or terminated, leaving teeth in an unfinished state that can be difficult or expensive to correct later. Interrupted treatment is not just a financial problem. It is a clinical one.

Here is what to do if you are struggling:

- Call the office early. Contact your orthodontic provider as soon as you know a payment is going to be late. Most offices have seen this before and would rather keep your treatment moving than lose a patient.

- Request a payment restructure. Many practices allow re-amortization of their in-house plans, meaning they can adjust payment amounts mid-treatment to fit a tighter budget without stopping care.

- Review your contract terms. Know what your agreement says about missed payments and default before a problem occurs. Some contracts include a grace period; others do not.

- Ask about a temporary pause with intent to resume. In genuine hardship cases, practices may pause treatment formally rather than terminate it, preserving your progress while you stabilize financially.

The orthodontic office is your partner in this. A proactive conversation is almost always more productive than avoiding the issue.

My honest take on financing orthodontic care

I have seen a lot of families walk into consultations financially unprepared, and it costs them. Not because the options are not there, but because nobody explained them in advance.

In my experience, the biggest missed opportunity is the upfront payment discount. Most people hear “$6,000 for braces” and immediately think about monthly payments. They never stop to ask whether paying in full saves money. When you can use an FSA to cover the balance tax-free, that 5 to 10% discount becomes even more significant.

The second thing I see overlooked is negotiation. People treat an orthodontist’s payment plan like a fixed price on a retail shelf. It is not. Offices genuinely want to complete your treatment. I have seen practices drop the required down payment, extend payment terms, and offer additional flexibility to families who simply asked directly and explained their situation honestly.

My honest advice: do your homework before the consultation. Know your insurance benefit maximum. Know your FSA contribution limit. Have a monthly payment number in mind that works for your budget. Walk in as a prepared decision-maker, not someone waiting to be told what everything will cost. That mindset shift changes every conversation you will have about orthodontic care for your family.

— Gloworthodontics

Flexible financing at Glow Orthodontics

At Gloworthodontics, serving families throughout Langley, British Columbia, flexible payment options are built into how care is delivered. The practice offers 0% in-house financing with monthly payment plans designed around real family budgets, and the team is experienced in helping patients coordinate insurance benefits, FSA funds, and payment schedules to minimize out-of-pocket costs. Whether you are exploring braces for your child or considering Invisalign for yourself, the consultation process includes a full breakdown of financing options tailored to your specific treatment plan. You can also explore the Invisalign treatment process to understand what clear aligner care involves before booking. Ready to get started? Book a consultation at gloworthodontics.ca and ask about current promotions.

FAQ

How much does orthodontic treatment typically cost?

Traditional braces generally range from $3,000 to $6,000, while Invisalign and clear aligners can run $4,500 to $10,000 depending on case complexity, treatment length, and location.

What is the easiest way to finance braces with no credit check?

In-house orthodontic payment plans typically require no credit check and offer 0% interest for 12 to 24 months, with a down payment of 20 to 30% of the total treatment cost.

Can I use my FSA or HSA for orthodontic treatment?

Yes. Both FSA and HSA funds can be applied to orthodontic expenses, including braces and Invisalign, and can reduce your effective cost by 20 to 30% through pre-tax savings.

Does dental insurance cover braces for adults?

Many dental insurance plans cover a portion of orthodontic treatment, though adult coverage is less common and may require proof of medical necessity. Coverage typically maxes out between $1,500 and $3,000 as a lifetime benefit.

What happens if I miss a payment during orthodontic treatment?

Missing payments can pause or terminate your treatment, leaving results incomplete. Contact your orthodontic office immediately to discuss re-amortizing your plan or adjusting the payment schedule before missing a payment if possible.