Braces Insurance: Navigating Coverage and Costs

December 9, 2025

Braces Insurance: Navigating Coverage and Costs

Over half of American families report financial stress when faced with orthodontic bills for braces. For many, the high price tag of a straighter smile can put goals like college savings or vacations on hold. Understanding how braces insurance coverage works could offer relief and smarter choices about your family’s health and budget. Discover what matters most when evaluating orthodontic coverage, from eligibility to hidden costs, so you can plan confidently and avoid unexpected expenses.

Table of Contents

- What Is Braces Insurance Coverage?

- Types Of Orthodontic Insurance Plans

- Eligibility And Covered Orthodontic Treatments

- How Claims And Reimbursements Work

- Out-Of-Pocket Expenses And Coverage Limits

- Comparing Braces Insurance With Alternatives

Key Takeaways

| Point | Details |

|---|---|

| Understanding Coverage | Braces insurance typically covers only medically necessary orthodontic treatments, often with age restrictions and lifetime maximums. |

| Types of Plans | Patients should evaluate different insurance types, such as PPO, DHMO, and direct reimbursement plans, for their specific needs. |

| Claims Process | A structured approach is necessary for orthodontic claims, including obtaining pre-authorization and tracking treatment progress. |

| Exploring Alternatives | In-house payment plans and dental discount plans can offer flexible financing options as alternatives to traditional insurance. |

What Is Braces Insurance Coverage?

Braces insurance coverage represents a specialized dental benefit that helps manage the potentially significant costs associated with orthodontic treatments. Understanding these insurance provisions is crucial for families considering orthodontic care, as treatment expenses can range from several thousand to tens of thousands of dollars.

Most dental insurance plans offer limited orthodontic coverage, typically with specific restrictions and conditions. Many dental plans cover orthodontics, but the coverage often differs from standard dental services. Generally, these plans focus on pediatric orthodontic treatments and impose lifetime dollar maximums on potential reimbursements. Specifically, insurers frequently provide coverage up to 50 percent of orthodontic charges, with a predetermined lifetime maximum benefit.

Insurance providers typically categorize orthodontic coverage into two primary categories: medically necessary treatments and elective cosmetic procedures. Medically necessary orthodontics often receive more comprehensive coverage, especially when addressing significant dental misalignments that could impact overall health. Medicare Parts A and B generally exclude orthodontic treatments unless deemed medically essential, which underscores the importance of understanding your specific insurance plan’s definitions and limitations.

Key aspects of braces insurance coverage usually include:

- Age restrictions (often limited to pediatric patients)

- Lifetime maximum benefit amounts

- Percentage of treatment costs covered

- Distinction between medical necessity and cosmetic procedures

- Waiting periods before coverage becomes active

- Specific documentation requirements for claims

Patients should carefully review their insurance policy details, consult directly with their insurance provider, and understand the exact terms of orthodontic coverage before beginning treatment. This proactive approach can help manage financial expectations and maximize potential insurance benefits.

Types of Orthodontic Insurance Plans

Understanding the various types of orthodontic insurance plans is crucial for patients seeking comprehensive dental coverage. The American Dental Association recognizes multiple insurance plan structures that offer different approaches to managing orthodontic expenses and patient care.

The most common orthodontic insurance plans include Preferred Provider Organization (PPO) Plans, which offer the most flexibility in choosing orthodontists. These plans typically provide coverage within a network of preferred providers while allowing patients to seek treatment outside the network at higher out-of-pocket costs. Dental Health Maintenance Organizations (DHMO) represent another significant insurance plan type, characterized by lower monthly premiums but more restricted provider networks and referral requirements.

Additional orthodontic insurance plan variations include:

- Dental Exclusive Provider Organization (EPO) Plans: Strict network limitations with no out-of-network coverage

- Indemnity Plans: Traditional insurance with predetermined reimbursement rates

- Direct Reimbursement Plans: Reimburse patients based on actual treatment expenses

- Discount or Referral Plans: Provide reduced rates through specific provider networks

Patients should carefully evaluate each plan’s specific features, including network restrictions, coverage percentages, lifetime maximums, and potential out-of-pocket expenses. Consulting with insurance providers and understanding the nuanced differences between plans can help individuals select the most appropriate orthodontic insurance coverage for their specific needs.

Eligibility and Covered Orthodontic Treatments

Eligibility for orthodontic insurance coverage is typically structured around specific medical and age-related criteria. Dental insurance plans frequently limit orthodontic benefits to cases of medical necessity, which means cosmetic treatments are often excluded from comprehensive coverage.

Medical Necessity is the primary determining factor for orthodontic treatment eligibility. Insurance providers generally require documented evidence of significant dental misalignments that could impact oral health, speech function, or overall physical well-being. Many dental plans cover orthodontics with specific limitations, typically focusing on pediatric patients and imposing lifetime dollar maximums. Common conditions that often qualify for coverage include:

- Severe malocclusion (significant bite misalignment)

- Dental crowding preventing proper cleaning

- Jaw structure abnormalities

- Speech impediments caused by dental misalignment

- Potential long-term health complications from untreated dental issues

The types of orthodontic treatments typically covered vary by insurance plan, but generally include:

- Traditional metal braces

- Ceramic braces

- Certain types of clear aligners

- Preliminary diagnostic procedures

- Initial consultation and treatment planning

Patients should carefully review their specific insurance policy, as coverage can differ dramatically between providers. Obtaining pre-authorization and comprehensive documentation from an orthodontic specialist is crucial for maximizing potential insurance benefits and understanding individual eligibility requirements.

How Claims and Reimbursements Work

Navigating the complex world of orthodontic insurance claims requires understanding the intricate process of reimbursement and payment structures. Dental plans typically distribute orthodontic benefits through a structured payment approach, which differs significantly from standard medical insurance procedures.

Initial Payment and Disbursement is a critical aspect of orthodontic insurance claims. Indemnity dental plans often reimburse patients based on a percentage of the total treatment charges, using a system referred to as ‘usual, customary, and reasonable’ (UCR) fees. Typically, insurance providers will make an initial payment at the beginning of active treatment (often called the ‘banding’ stage) and then distribute the remaining balance over the course of the treatment, which can extend up to 18 months.

The claims and reimbursement process typically involves several key steps:

- Obtaining a comprehensive treatment plan from an orthodontist

- Submitting pre-authorization documentation to the insurance provider

- Receiving initial approval and coverage determination

- Tracking treatment progress and submitting periodic claims

- Managing out-of-pocket expenses and potential co-payments

Patients should maintain detailed records of all orthodontic procedures, communications with insurance providers, and treatment documentation. Understanding the specific reimbursement mechanisms of your insurance plan can help minimize unexpected expenses and maximize your potential coverage benefits. It’s crucial to work closely with both your orthodontic provider and insurance company to ensure smooth claims processing and optimal financial management of your orthodontic treatment.

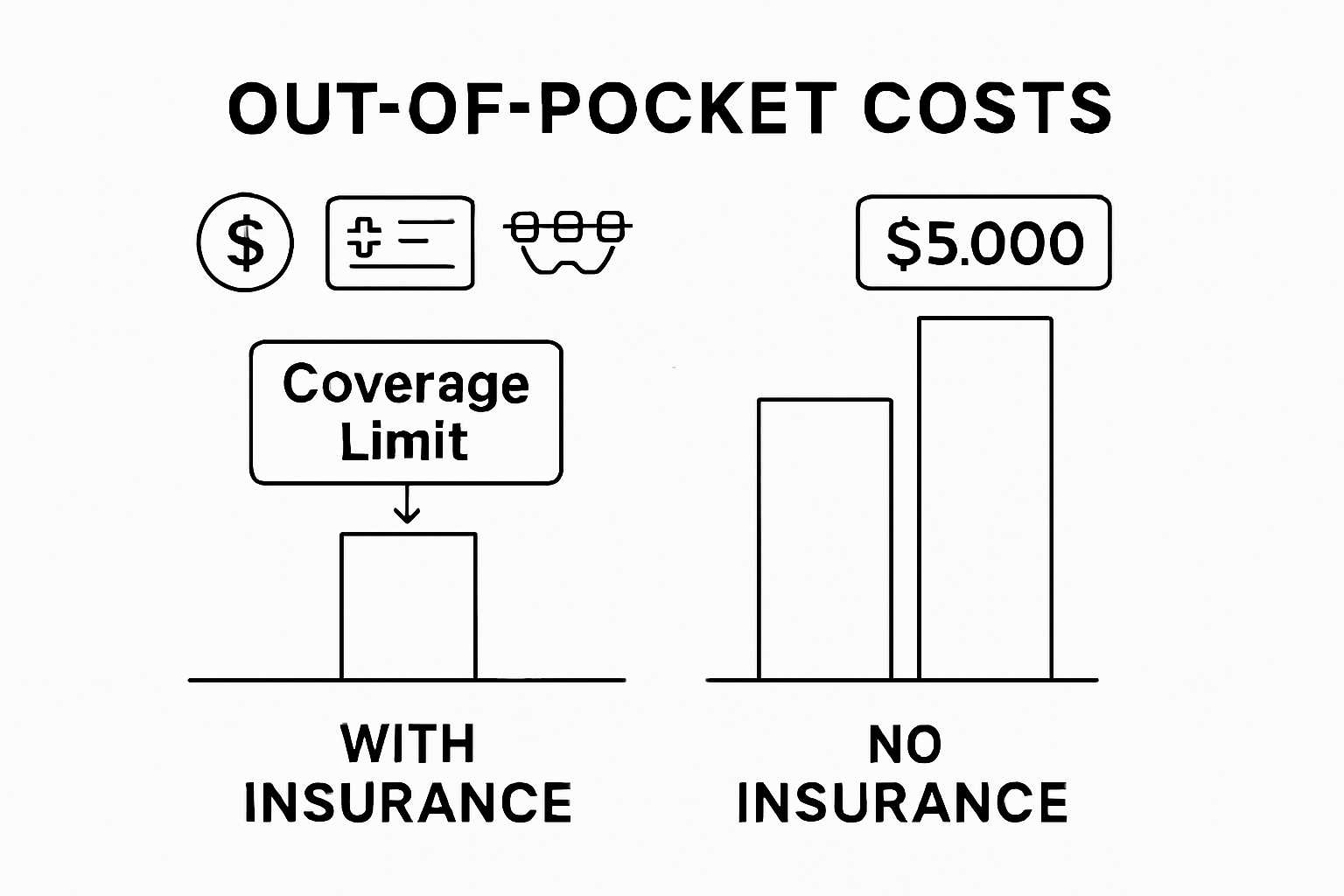

Out-of-Pocket Expenses and Coverage Limits

Navigating the financial landscape of orthodontic treatment requires a thorough understanding of potential out-of-pocket expenses and insurance coverage limitations. Even with dental insurance, patients will most likely encounter significant personal financial responsibilities, making comprehensive planning essential for managing treatment costs.

Coverage Limitations play a critical role in determining patient expenses. Dental insurance policies frequently exclude cosmetic procedures and impose strict requirements for medical necessity, which can dramatically impact overall treatment affordability. Typical out-of-pocket expenses include:

- Deductibles not covered by insurance

- Copayments for initial and follow-up treatments

- Expenses beyond the lifetime maximum benefit

- Costs for specialized or advanced orthodontic procedures

- Additional diagnostic tests or preliminary treatments

Patients should anticipate that most dental plans cover approximately 50 percent of orthodontic charges, with a predetermined lifetime maximum. This means individuals might need to budget for substantial personal expenses, especially for complex treatments or those extending beyond standard coverage parameters. Strategies for managing these costs include:

- Exploring flexible spending accounts

- Investigating payment plans offered by orthodontic offices

- Comparing multiple insurance providers

- Considering treatments that align more closely with insurance coverage requirements

Careful financial planning and a detailed understanding of your specific insurance policy can help minimize unexpected expenses and make orthodontic treatment more financially manageable. Always request a comprehensive breakdown of potential costs and coverage from both your insurance provider and orthodontic specialist.

Comparing Braces Insurance With Alternatives

Patients seeking orthodontic treatment have multiple financial options beyond traditional insurance coverage, each with unique advantages and considerations. Understanding these alternatives can help individuals make informed decisions about managing their orthodontic expenses.

In-House Payment Plans represent a flexible alternative to standard insurance. Many orthodontic practices offer customized installment plans directly managed by their offices, typically requiring an initial down payment and spreading remaining costs over the treatment duration. These plans often provide benefits such as zero-interest financing, personalized payment schedules, and direct negotiation with the provider.

Alternative financing options for orthodontic treatment include:

- Dental Discount Plans: Provide reduced rates on treatments

- Health Savings Accounts (HSAs): Allow tax-advantaged medical expense funding

- Flexible Spending Accounts (FSAs): Permit pre-tax dollar allocation for medical costs

- State Medicaid programs and dental school treatment options, especially for low-income patients or seniors

- Personal loans or medical credit lines

Patients should carefully evaluate each alternative’s total cost, flexibility, and potential long-term financial implications. Consulting with orthodontic offices and financial advisors can help identify the most cost-effective approach tailored to individual financial circumstances and treatment requirements.

Take Control of Your Braces Insurance and Treatment Costs Today

Understanding braces insurance coverage can feel overwhelming with all the rules about medical necessity, coverage limits, and out-of-pocket expenses. Many patients worry about navigating claim processes or facing unexpected costs despite insurance. Glow Orthodontics is here to guide you through every step with personalized treatment options that fit your unique situation and budget.

Explore how our caring team in Langley, British Columbia, helps you maximize your insurance benefits while providing transparent cost estimates. Whether you qualify under medical necessity criteria or need flexible payment plans, our goal is to deliver your best smile without financial stress. Visit Glow Orthodontics now to schedule your consultation and discover tailored solutions. Don’t wait to understand your coverage and start your journey toward a glowing smile with confidence.

Frequently Asked Questions

What is braces insurance coverage?

Braces insurance coverage is a specific dental benefit designed to help manage the costs associated with orthodontic treatments, which can range from several thousand to tens of thousands of dollars.

What types of orthodontic insurance plans are available?

Common orthodontic insurance plans include Preferred Provider Organization (PPO) Plans, Dental Health Maintenance Organizations (DHMO), Dental Exclusive Provider Organization (EPO) Plans, Indemnity Plans, Direct Reimbursement Plans, and Discount or Referral Plans. Each offers different levels of coverage and flexibility.

What orthodontic treatments are typically covered by insurance?

Generally covered treatments include traditional metal braces, ceramic braces, certain clear aligners, preliminary diagnostic procedures, and initial consultation and treatment planning, depending on the specific insurance plan.

How do claims and reimbursements work for orthodontic insurance?

The claims process involves obtaining a treatment plan from an orthodontist, submitting pre-authorization documentation, and receiving payments based on a percentage of total charges. Patients usually pay part of the costs upfront, with remaining payments distributed throughout the treatment period.