Does HSA Cover Invisalign? Real Benefits for Parents

January 5, 2026

Does HSA Cover Invisalign? Real Benefits for Parents

Every parent wants the best smile for their teenager, but orthodontic bills for Invisalign can leave families searching for answers. With more than 80 percent of American families using health spending accounts to manage rising medical costs, understanding what Health Savings Accounts actually cover is essential. Parents in Langley, BC need clarity on how these accounts work and whether they can use HSA funds for orthodontic care. This guide gives practical insights that make a real difference when planning for your child’s dental future.

Table of Contents

- What Is HSA and How Does It Work?

- Types of Health Spending Accounts Explained

- Is Invisalign an HSA-Eligible Orthodontic Expense?

- Common HSA Coverage Rules and Misconceptions

- Maximizing HSA Funds for Your Child’s Invisalign

- Comparing HSA, FSA, and Insurance for Orthodontics

Key Takeaways

| Point | Details |

|---|---|

| Tax Advantages of HSAs | HSAs offer a triple tax benefit: contributions reduce taxable income, account growth is tax-free, and withdrawals for qualified medical expenses are tax-free. |

| Flexibility and Portability | HSAs are individually owned and portable, allowing individuals to maintain their account when changing jobs or insurance plans. |

| Understanding Account Types | Different health spending accounts (HSAs, FSAs, HRAs) come with unique features and rules, impacting how individuals can manage their medical expenses. |

| Strategic Use for Orthodontics | Parents can utilize HSAs effectively for orthodontic treatments like Invisalign, leveraging tax advantages while managing out-of-pocket expenses. |

What Is HSA and How Does It Work?

A Health Savings Account (HSA) represents a powerful financial tool designed specifically for managing healthcare expenses while offering unique tax advantages. Defined by healthcare regulations, HSAs are specialized savings accounts paired with high-deductible health plans (HDHPs) that allow individuals to set aside money for medical costs in a tax-efficient manner.

The fundamental mechanics of an HSA involve three primary financial benefits. First, contributions are made with pre-tax dollars, which immediately reduces your taxable income. Second, the money in your account grows tax-free through potential investments or interest earnings. Third, withdrawals for qualified medical expenses are completely tax-free, creating a triple tax advantage that distinguishes HSAs from other savings vehicles. According to IRS Publication 969, these accounts are individually owned and remain portable, meaning you can keep the account even if you change jobs or health insurance providers.

To qualify for an HSA, you must be enrolled in a high-deductible health plan that meets specific IRS guidelines. These plans typically have lower monthly premiums but higher out-of-pocket expenses before insurance coverage begins. Contribution limits are set annually by the IRS, with separate maximums for individual and family coverage. Funds in an HSA can cover a wide range of medical expenses, including:

- Deductibles

- Copayments

- Prescription medications

- Certain medical equipment

- Some dental and vision expenses

Pro tip: Consider maxing out your HSA contributions each year, as unused funds roll over indefinitely and can serve as an additional retirement savings vehicle.

Here is a summary of how HSAs provide financial advantages compared to traditional savings accounts:

| Feature | Health Savings Account (HSA) | Regular Savings Account |

|---|---|---|

| Tax Benefits | Triple tax advantage | Interest taxed as income |

| Medical Use | Fund medical expenses tax-free | No special medical use |

| Portability | Remains with account holder | No portability restrictions |

| Investment Growth | Grows tax-free | Taxed on gains |

Types of Health Spending Accounts Explained

Health spending accounts are specialized financial tools designed to help individuals manage medical expenses more efficiently. According to healthcare guidelines, there are three primary types of health spending accounts: Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), and Health Reimbursement Arrangements (HRAs). Each account type offers unique features and tax advantages tailored to different healthcare and employment scenarios.

Health Savings Accounts (HSAs) stand out as the most flexible option for individuals. These accounts require enrollment in a high-deductible health plan and offer triple tax benefits: contributions are made with pre-tax dollars, funds grow tax-free, and withdrawals for qualified medical expenses are not taxed. IRS Publication 969 highlights that HSAs are individually owned and portable, meaning you can maintain the account regardless of job changes or insurance transitions.

Flexible Spending Accounts (FSAs) are employer-established accounts with different rules. These accounts allow employees to set aside pre-tax dollars for medical expenses, but typically operate on a ‘use it or lose it’ principle. Most FSAs require participants to spend their allocated funds within the plan year or forfeit the remaining balance. Common eligible expenses include:

- Prescription medications

- Medical copayments

- Dental treatments

- Vision care expenses

- Certain medical supplies

Health Reimbursement Arrangements (HRAs) differ from other accounts as they are entirely employer-funded. Companies provide these accounts to reimburse employees for specific medical expenses, with contribution and usage rules determined by the employer. Unlike HSAs and FSAs, employees cannot contribute their own funds to HRAs.

The primary differences between these accounts can be summarized in a comparison table:

| Account Type | Ownership | Contribution Source | Fund Rollover | Tax Benefits |

|---|---|---|---|---|

| HSA | Individual | Individual/Employer | Full Rollover | Triple Tax |

| FSA | Employer | Employee | Limited | Pre-tax Contributions |

| HRA | Employer | Employer Only | Employer Defined | Reimbursement Based |

Pro tip: Carefully review your specific health plan and employment benefits to determine which health spending account provides the most advantageous financial strategy for your personal healthcare needs.

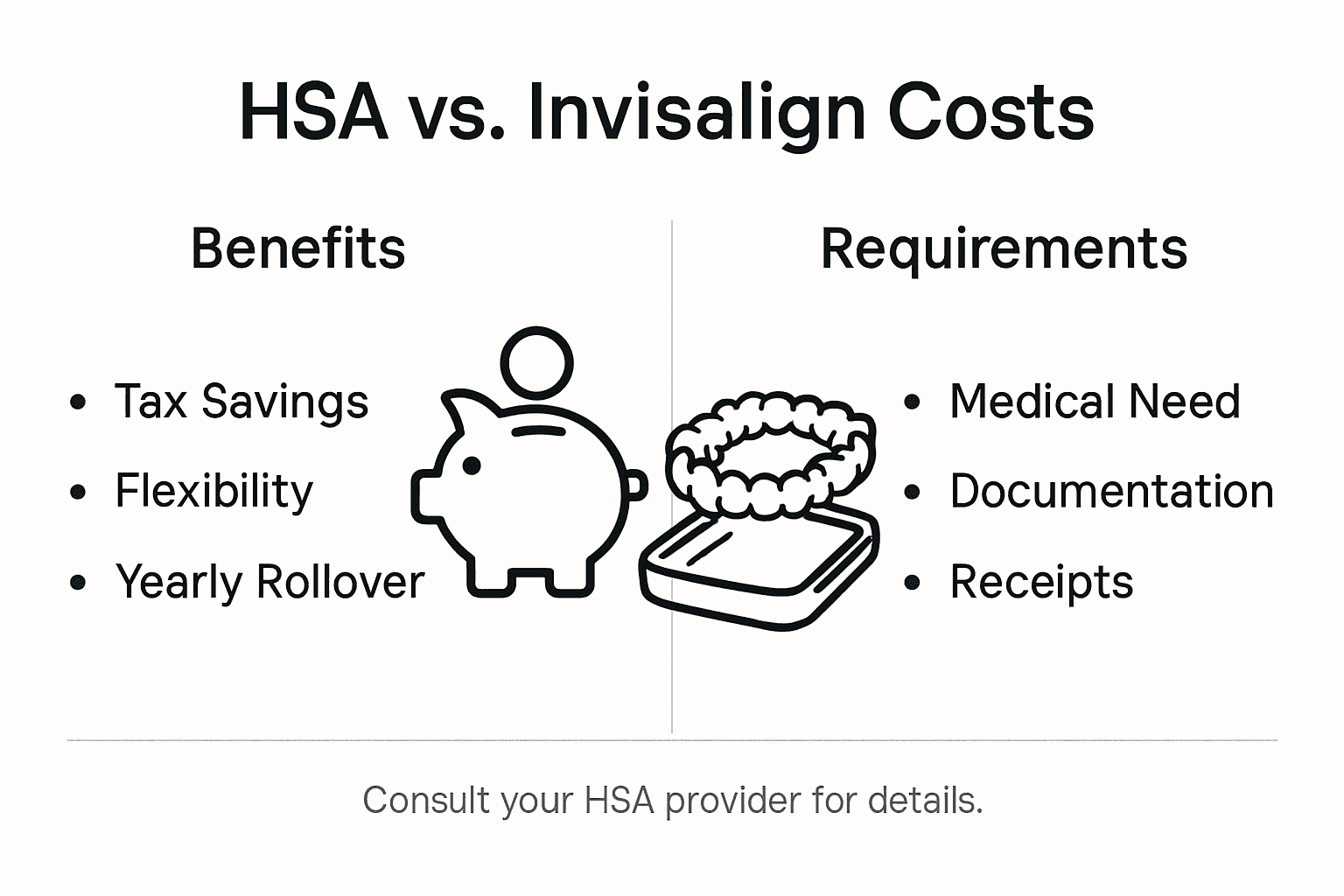

Is Invisalign an HSA-Eligible Orthodontic Expense?

Parents seeking orthodontic solutions for their children often wonder about the financial implications of treatments like Invisalign. According to HSA eligibility guidelines, Invisalign is indeed considered a qualified medical expense that can be paid using Health Savings Account (HSA) funds. This means families can leverage their tax-advantaged accounts to help cover the cost of orthodontic treatment, potentially reducing their out-of-pocket expenses.

Orthodontic treatments fall under a specific category of medical expenses recognized by the Internal Revenue Service. Congressional research confirms that expenses related to diagnosis, cure, mitigation, treatment, or prevention of disease are eligible for HSA funding. Invisalign specifically qualifies because it addresses dental misalignment, which is considered a medical condition that impacts overall oral health and function.

To use HSA funds for Invisalign, several key requirements must be met:

- The account holder must be enrolled in a high-deductible health plan

- The treatment must be recommended by a qualified healthcare professional

- The expense must be considered medically necessary, not purely cosmetic

- Documentation from your orthodontist proving medical necessity should be retained

It’s important to note that while Invisalign is HSA-eligible, the entire treatment cost might not be covered if it’s considered primarily aesthetic. Orthodontists typically provide documentation explaining the medical necessity of the treatment, which is crucial for HSA reimbursement.

Pro tip: Always consult with your orthodontist and HSA administrator to confirm the specific documentation required for Invisalign treatment reimbursement, and keep detailed records of all medical expenses.

Below is a quick reference table outlining the typical documentation needed for orthodontic HSA reimbursement:

| Requirement | Purpose | Recommended Documentation |

|---|---|---|

| Medical Necessity | Confirms eligibility | Letter from orthodontist |

| Treatment Receipt | Proves expense payment | Itemized invoice |

| Treatment Plan | Details procedure and cost | Written plan from provider |

Common HSA Coverage Rules and Misconceptions

Health Savings Accounts (HSAs) come with a complex set of rules that often confuse account holders. According to IRS guidelines, there are specific requirements and limitations that many people misunderstand. The fundamental rule is that to contribute to an HSA, you must be enrolled in a high-deductible health plan and have no other disqualifying health coverage, which surprises many potential account holders.

Qualified medical expenses form the cornerstone of HSA usage. Financial regulatory research highlights that not all healthcare expenses are eligible for tax-free withdrawal. Common misconceptions exist about what expenses truly qualify, leading many account holders to make costly mistakes. The IRS maintains a specific list of eligible expenses, which includes:

- Prescription medications

- Dental treatments

- Vision care

- Certain medical equipment

- Orthodontic treatments

- Mental health counseling

- Laboratory fees

One of the most significant misunderstandings involves the account’s flexibility. Contrary to popular belief, HSA funds are not ‘use it or lose it’ like Flexible Spending Accounts (FSAs). These funds roll over completely from year to year, allowing long-term savings and investment. Additionally, HSAs are entirely portable – meaning you can keep the account even if you change jobs or health insurance providers, which provides unprecedented financial freedom.

Penalties and tax implications represent another critical area of confusion. Withdrawals for non-qualified expenses before age 65 incur a 20% penalty plus income tax. After age 65, non-medical withdrawals are taxed as regular income without additional penalties, essentially transforming the HSA into a supplemental retirement account.

Pro tip: Maintain meticulous records of all medical expenses and HSA transactions, as documentation is crucial for potential future audits and ensuring compliance with IRS regulations.

Maximizing HSA Funds for Your Child’s Invisalign

Parents facing the significant expense of Invisalign treatment have a powerful financial tool at their disposal: the Health Savings Account (HSA). According to HSA funding guidelines, strategic planning can help families leverage these accounts to make orthodontic care more affordable. The triple tax advantage of HSAs – tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses – makes them an ideal resource for managing Invisalign costs.

Orthodontic treatment planning requires a long-term financial approach. Orthodontic experts recommend spreading HSA contributions over the entire treatment duration to manage the substantial out-of-pocket expenses associated with Invisalign. Consider these strategic steps for maximizing your HSA funds:

- Estimate the total Invisalign treatment cost in advance

- Calculate annual contribution amounts to cover treatment

- Coordinate HSA funds with any available dental insurance

- Keep detailed documentation of all treatment expenses

- Plan for potential additional orthodontic costs

The unique benefit of HSAs is their flexibility and long-term savings potential. Unlike other healthcare accounts, HSA funds roll over completely from year to year, allowing parents to accumulate funds for multi-year orthodontic treatments. This means you can start saving well before your child’s treatment begins, potentially covering a significant portion of the expenses without financial strain.

Timing is crucial when using HSA funds for Invisalign. Most orthodontic treatments for teenagers span 12-24 months, so parents should plan their HSA contributions accordingly. By contributing the maximum allowed amount annually and strategically managing these funds, families can substantially reduce the out-of-pocket expenses for their child’s orthodontic care.

Pro tip: Consult with both your orthodontist and HSA administrator to confirm precise documentation requirements and ensure smooth reimbursement for your child’s Invisalign treatment.

Comparing HSA, FSA, and Insurance for Orthodontics

Parents navigating orthodontic expenses face multiple financial options, each with unique advantages and limitations. According to orthodontic association research, Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), and dental insurance represent three distinct strategies for managing Invisalign and braces costs.

Financing mechanisms for orthodontic care vary significantly. Risk management research reveals critical differences between these options. Here’s a comprehensive breakdown of each approach:

HSA Advantages:

- Funds roll over annually

- Triple tax benefit

- Can be invested

- Individually owned

- No strict spending deadlines

FSA Characteristics:

- Employer-established

- Annual contribution limits

- ‘Use it or lose it’ policy

- No investment options

- Immediate tax savings

Dental Insurance Considerations:

- Partial coverage for orthodontics

- Often age-restricted

- Lifetime maximum benefit

- Predetermined percentage of cost

- Specific network requirements

Optimal financial planning involves strategic combination of these resources. Some families might use dental insurance as a primary coverage, supplement with FSA funds for immediate tax advantages, and leverage HSA accounts for long-term, flexible healthcare spending. This multi-layered approach can significantly reduce out-of-pocket expenses for comprehensive orthodontic treatment.

Pro tip: Calculate your total expected orthodontic expenses and map out a comprehensive funding strategy that maximizes tax benefits and minimizes your financial burden.

Make Invisalign Affordable with Your HSA at Glow Orthodontics

Parents seeking effective orthodontic care for their children often face the challenge of managing the high costs associated with Invisalign treatment. This article highlights how Health Savings Accounts (HSAs) can be a vital tool to ease that financial burden by offering triple tax advantages and covering qualified expenses like Invisalign when medically necessary. At Glow Orthodontics, we understand these concerns and are dedicated to helping families make the most of their healthcare spending accounts.

Take control of your child’s smile journey today by exploring personalized Invisalign options at Glow Orthodontics. Our professional and compassionate team in Langley, British Columbia will guide you through the treatment process and help maximize your HSA benefits. Schedule a consultation now through our easy online booking system and get one step closer to a confident, glowing smile. Visit Glow Orthodontics to learn more and book your appointment.

Discover how our comprehensive orthodontic care can work hand-in-hand with your HSA at Glow Orthodontics. Start your smile transformation by contacting us today.

Frequently Asked Questions

Does HSA cover Invisalign treatments?

Yes, Invisalign is considered a qualified medical expense that can be paid using Health Savings Account (HSA) funds, as long as it meets the necessary requirements for medical necessity.

What documentation is needed to use HSA funds for Invisalign?

You will need documentation from your orthodontist confirming the medical necessity for the treatment, an itemized receipt of the expense, and a treatment plan detailing the costs involved.

Are there any penalties for using HSA funds for non-qualified expenses like cosmetic treatments?

Yes, if HSA funds are used for non-qualified expenses before age 65, there is a 20% penalty plus income tax on the amount withdrawn. After age 65, only the income tax applies.

How can I maximize HSA contributions for my child’s Invisalign treatment?

To maximize HSA funds for Invisalign, estimate the total treatment cost, plan your annual contributions accordingly, and utilize any available dental insurance to supplement costs while keeping detailed records for reimbursement.