Does state insurance cover braces in BC? Key facts

March 6, 2026

Does state insurance cover braces in BC? Key facts

Many parents assume British Columbia’s state insurance fully covers braces for their children, but that’s rarely the case. MSP, the province’s Medical Services Plan, only covers orthodontic treatment when it’s medically necessary due to severe conditions like cleft palate or jaw deformities. For most families seeking routine orthodontic care, coverage is limited or nonexistent. This guide explains what MSP actually covers, which provincial assistance programs might help, and how private insurance fits into the equation, so you can plan financially and avoid costly surprises.

Table of Contents

- Understanding State Insurance Coverage In BC

- Provincial Assistance Programs For Orthodontics

- Eligibility And Medical Necessity Criteria

- Comparing Public And Private Insurance Coverage

- Common Misconceptions About State Insurance

- Understanding Treatment Costs And Financial Planning

- Applying For Coverage And Subsidies

- Practical Tips For Parents Navigating Insurance

- Explore Orthodontic Care Solutions At Glow Orthodontics

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| MSP limits | MSP only covers medically necessary braces, excluding routine cosmetic cases. |

| Provincial aid | The Children’s Oral Health Program helps eligible low-income families with orthodontic costs. |

| Private insurance | Private plans cover 25-50% of costs with lifetime caps between $3,000-$5,000. |

| Eligibility matters | Specialist referrals and documented medical necessity determine coverage approval. |

| Plan ahead | Understanding coverage scope prevents financial surprises and helps families budget effectively. |

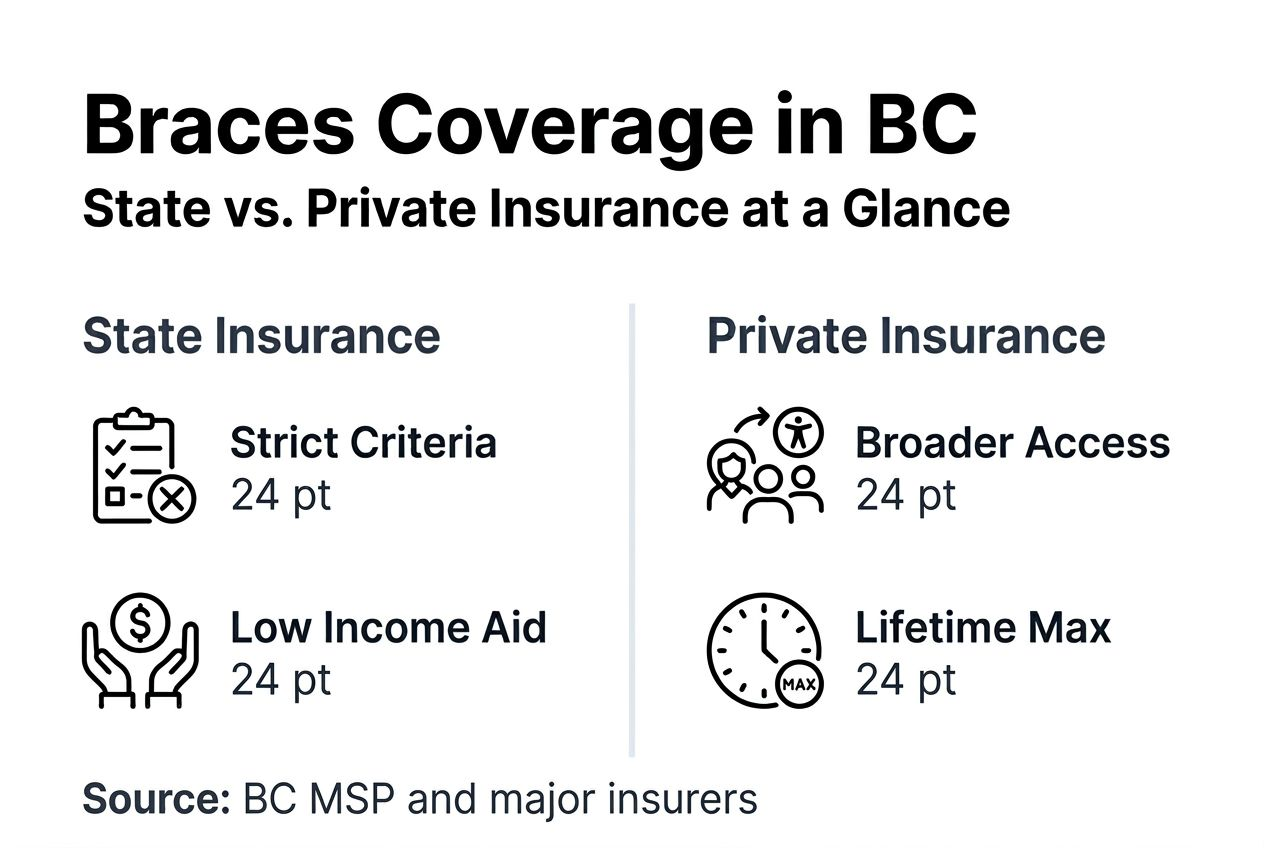

Understanding state insurance coverage in BC

British Columbia’s Medical Services Plan primarily covers basic medical services and certain dental surgeries, but routine orthodontics rarely make the list. MSP excludes routine braces except medically necessary cases, meaning your child’s crooked teeth alone won’t qualify unless they’re causing serious functional problems.

Medical necessity is the key term here. It means braces are required to address conditions like cleft palate, severe malocclusion affecting eating or speech, or significant jaw deformities. You’ll need a specialist referral and detailed assessment to prove the treatment isn’t just cosmetic. Most standard orthodontic treatments that improve appearance or prevent minor dental issues fall outside MSP’s scope.

Knowing these limits upfront helps you prepare financially and explore other support options. If you’re considering braces coverage in BC, understanding MSP’s strict criteria is your first step. Without meeting medical necessity standards, families must rely on provincial assistance programs or private insurance to manage costs.

Key exclusions from MSP coverage include:

- Braces for cosmetic or routine alignment purposes

- Preventive orthodontic treatments for minor crowding

- Retainers and follow-up appliances unless medically required

- Initial consultations for non-medical cases

Provincial assistance programs for orthodontics

While MSP has strict limits, BC offers targeted programs to help low-income families afford orthodontic care. The Children’s Oral Health Program provides assistance to eligible low-income families for dental and some orthodontic treatments, sometimes covering partial or full costs depending on medical need and financial status.

These subsidies require proof of low income and that treatment is medically necessary. You’ll need to submit income verification documents, specialist reports, and detailed treatment plans. The application process takes time, so start early to avoid delaying your child’s care. Programs can significantly reduce out-of-pocket expenses, but they’re not available to everyone.

Awareness of these programs is crucial for families struggling with the cost of braces in BC. Even if you don’t meet all criteria, understanding what’s available helps you explore every funding avenue. Work closely with your orthodontist’s office to identify which programs you might qualify for and gather necessary documentation.

Steps to access provincial assistance:

- Verify income eligibility thresholds for the Children’s Oral Health Program

- Obtain a specialist referral confirming medical necessity

- Collect required documentation including income statements and tax returns

- Submit applications well before planned treatment start dates

- Follow up regularly with program administrators

Eligibility and medical necessity criteria

Securing state insurance or subsidy coverage hinges on meeting strict eligibility standards. Orthodontic coverage requires a formal diagnosis of a medically necessary condition, not just aesthetic concerns. MSP requires specialist referral and documented medical necessity for orthodontic coverage, making proper documentation essential.

Medical necessity involves functional impairments that affect your child’s health. Think jaw deformities causing pain, cleft palate requiring surgical correction, or severe malocclusion interfering with eating or speech. Mild crowding or minor bite issues won’t qualify. Your orthodontist must provide detailed reports explaining how the condition impacts daily function and why treatment is medically required, not elective.

Financial assistance programs also have income thresholds. Most subsidies target families below specific income levels, verified through tax documents and pay stubs. Meeting both medical and financial criteria improves approval chances, but accurate documentation and early consultation are critical. Understanding eligibility for braces insurance helps you prepare the right paperwork from the start.

Steps to establish medical necessity:

- Schedule an evaluation with an orthodontic specialist

- Request detailed written reports documenting functional impairments

- Gather supporting evidence like X-rays and dental models

- Obtain formal specialist referrals for MSP or subsidy applications

- Keep copies of all medical documentation for your records

Comparing public and private insurance coverage

Public and private insurance serve different roles in covering orthodontic costs. Public insurance through MSP covers only medically necessary braces, offering zero coverage for cosmetic cases. Meanwhile, private dental insurance covers 25% to 50% of orthodontic costs, with lifetime maximums typically between $3,000 and $5,000.

Private plans vary widely in coverage percentages, waiting periods, and lifetime caps. Some families use both public programs for medically necessary cases and private insurance for braces to reduce overall costs. However, out-of-pocket expenses often remain substantial even with dual coverage. Understanding both coverage types helps you plan realistically for the financial responsibility ahead.

Most insurance options for braces include annual maximums and waiting periods before orthodontic benefits kick in. If you’re considering private dental insurance coverage, review policy details carefully to understand what’s included and excluded. Some plans cover traditional braces but not Invisalign, while others have age restrictions.

| Coverage Type | Eligibility | Typical Coverage | Limitations |

|---|---|---|---|

| MSP (Public) | Medically necessary cases only | Full coverage for approved treatments | Strict medical criteria, excludes cosmetic care |

| Provincial Subsidies | Low-income families | Partial to full coverage | Income and medical necessity requirements |

| Private Insurance | Policyholders with dental plans | 25-50% of costs | Lifetime caps of $3,000-$5,000, waiting periods |

| Out-of-Pocket | All families | Remaining balance | Can be substantial even with insurance |

Pro Tip: Review your private insurance policy annually to understand changes in coverage limits and maximize benefits before they reset.

Common misconceptions about state insurance

Many parents mistakenly believe MSP fully covers routine orthodontic treatments for children. In reality, MSP covers only medically necessary cases, excluding most cosmetic braces. This misconception leads families to assume costs will be minimal, only to face unexpected bills when treatment begins.

Another widespread myth is that private insurance covers full orthodontic treatment costs. Private insurance covers partial costs with limits and lifetime maximums, leaving families responsible for significant portions. Some parents also believe state subsidies are available to all families regardless of income, but subsidies require income-based eligibility and extensive documentation.

Clarifying these myths helps parents set realistic expectations and plan accordingly. Understanding braces coverage myths prevents financial surprises and allows you to explore all available funding sources early in the treatment planning process.

Common misconceptions debunked:

- MSP covers all children’s braces: False. Only medically necessary cases qualify.

- Private insurance eliminates out-of-pocket costs: False. Coverage is partial with caps.

- Provincial subsidies are automatic: False. You must apply and meet strict criteria.

- Orthodontic coverage is the same as dental coverage: False. Orthodontics often have separate limits.

Understanding treatment costs and financial planning

Orthodontic treatment costs in BC typically range from $3,000 to $8,000 depending on case complexity, treatment duration, and appliance type. You’ll need to budget for costs not covered by MSP or subsidies, including initial consultations, appliances, adjustments, and follow-up care. These expenses add up quickly without proper planning.

Leverage provincial subsidies, private insurance, and payment plans offered by orthodontic practices to reduce immediate financial burden. Many orthodontists provide flexible payment options that spread costs over the treatment period. Early financial planning prevents surprises and facilitates a smoother treatment experience for your family.

Understanding the cost of braces in BC helps you budget accurately. If you’re considering alternatives, research using insurance for Invisalign coverage since some private plans cover clear aligners differently than traditional braces. Maintain clear communication with your orthodontist about costs and insurance processes to avoid confusion.

Financial planning strategies:

- Request detailed cost estimates before starting treatment

- Explore payment plans that fit your budget

- Maximize private insurance benefits by timing treatment strategically

- Apply for provincial subsidies well in advance

- Set aside emergency funds for unexpected orthodontic needs

Pro Tip: Ask your orthodontist about in-house financing options or third-party payment plans that offer low or no interest for qualified families.

Applying for coverage and subsidies

Securing coverage starts with confirming medical necessity through an orthodontic specialist early in the process. Your specialist will conduct thorough assessments and provide detailed reports needed for MSP or subsidy applications. Timing matters, as applicants must submit income verification and medical documentation to access subsidies, and processing takes weeks or months.

Gather required documents including referral letters, specialist reports, income proof like tax returns and pay stubs, and treatment plans. Submit applications to provincial programs well before your child’s planned treatment start date to avoid delays. Missing documentation or incomplete applications can push back approval and delay care.

Work closely with your orthodontist’s office for accurate claim submissions. Their billing staff understands insurance requirements and can help you navigate paperwork. Follow up regularly on application status and be ready to provide additional documentation if requested. For help with document verification guidelines, consult resources that explain proper attestation and notarization.

Application steps:

- Schedule specialist evaluation and obtain medical necessity documentation

- Collect all required financial records and income verification

- Complete application forms thoroughly and accurately

- Submit applications at least 8-12 weeks before treatment starts

- Track application status and respond promptly to requests

- Confirm approval and coverage details before beginning treatment

Get tips for navigating insurance claims from your orthodontist’s team to streamline the process.

Practical tips for parents navigating insurance

Leverage your orthodontist’s support in submitting and tracking insurance claims. Their billing specialists handle claims daily and understand common pitfalls. They can pre-authorize treatments, submit required documentation, and follow up with insurers on your behalf, reducing your administrative burden significantly.

Understand common insurance terms like deductibles, co-pays, lifetime maximums, and waiting periods to avoid misunderstandings. Knowing what these mean helps you interpret coverage documents and ask informed questions. Plan treatment timing to align with insurance coverage windows and subsidy approvals, maximizing benefits available in each calendar year.

Keep detailed records of all healthcare and financial documents related to orthodontic care. Maintain files with copies of referrals, specialist reports, insurance claims, payment receipts, and correspondence with insurers or subsidy programs. This organization simplifies future claims and provides evidence if disputes arise.

Communicate openly with your orthodontist’s billing staff for guidance on coverage nuances. They can explain what your specific plan covers and suggest strategies to maximize benefits. Building this partnership makes the insurance process less stressful and more successful.

Actionable insurance navigation tips:

- Request pre-authorization from insurers before starting treatment

- Understand your policy’s orthodontic exclusions and limitations

- Track annual maximums and plan treatments accordingly

- Keep copies of all submitted claims and approvals

- Set calendar reminders for reapplication deadlines

Pro Tip: Schedule your initial consultation near the start of your insurance year to maximize coverage across the full treatment period. Learn more practical insurance tips for braces to optimize your family’s benefits.

Explore orthodontic care solutions at Glow Orthodontics

Navigating insurance and coverage can feel overwhelming, but you don’t have to do it alone. Glow Orthodontics offers expert orthodontic care tailored for children and teens, with a team experienced in helping families understand insurance options and financial planning. They work with you to maximize available coverage and create payment plans that fit your budget.

Explore treatment options including traditional braces and Invisalign, each designed to meet your child’s unique needs. Whether you’re just starting to research options or ready to schedule a consultation, Glow Orthodontics provides personalized support throughout the journey. Their team helps you navigate complex coverage questions and ensures you understand all costs upfront.

Check out the Orthodontic care for teens guide and Invisalign treatment process guide for detailed resources. Contact Glow Orthodontics today to schedule a consultation and discover how they can help your family achieve beautiful smiles while managing costs effectively.

Frequently asked questions

Does MSP cover braces for cosmetic reasons in BC?

No, MSP does not cover braces for cosmetic purposes. Coverage is limited to medically necessary orthodontic treatments addressing severe functional impairments like cleft palate or jaw deformities affecting eating and speech.

What income level qualifies for provincial orthodontic subsidies?

Income eligibility varies by program, but the Children’s Oral Health Program typically targets low-income families. Check current income thresholds on the BC Ministry of Health website and gather tax documents to verify eligibility.

Can I use both MSP and private insurance for my child’s braces?

Yes, if your child’s treatment qualifies as medically necessary under MSP, you can also use private insurance for additional costs. However, MSP coverage is rare, so most families rely primarily on private plans and out-of-pocket payments.

How long does it take to get subsidy approval in BC?

Subsidy approval typically takes 8 to 12 weeks after submitting a complete application. Submit applications well before your planned treatment start date to avoid delays in care.

What documents do I need to apply for orthodontic subsidies?

You’ll need specialist referrals, detailed medical reports documenting necessity, income verification like tax returns and pay stubs, and completed application forms. Keep copies of all submissions for your records.

Recommended

- Braces & Insurance in Langley: Your Complete Guide | 2025

- Braces Insurance: Navigating Coverage and Costs – RG API

- Braces Coverage in Langley: Your Guide | Glow Orthodontics

- Travel with Braces: Tips & Tricks | Glow Orthodontics

- Tratamentul ortodontic: Cum influențează sănătatea copilului | Lucilla Dental Clinic | cabinet stomatologic Bucuresti sector 4 | stomatologie Bucuresti