Health insurance that covers braces: Langley parents’ guide

March 10, 2026

Health insurance that covers braces: Langley parents’ guide

Many Langley parents assume British Columbia’s Medical Services Plan covers braces for their children. Unfortunately, that’s not the case. Orthodontic treatment typically costs thousands of dollars without proper coverage, making private dental insurance essential. This guide explains how coverage works, what plans actually pay for, and how to choose affordable insurance that fits your family’s orthodontic needs in 2026.

Table of Contents

- Understanding Orthodontic Coverage In Canadian Health Insurance

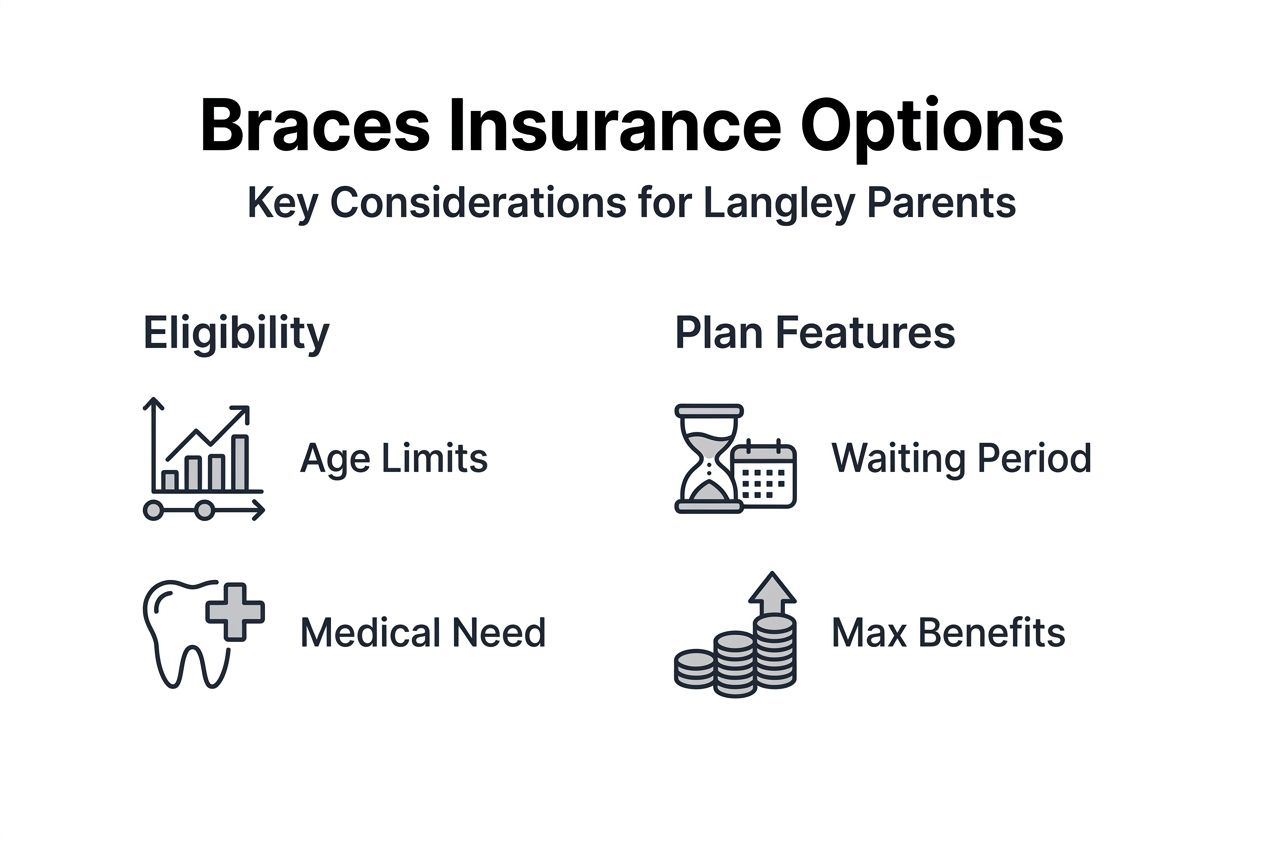

- Age Eligibility And Medical Necessity For Orthodontic Coverage

- Common Exclusions, Waiting Periods, And Policy Limits

- Debunking Common Misconceptions About Insurance And Braces

- Comparing Dental Insurance Plans For Orthodontic Benefits In BC

- Practical Steps To Maximize Your Orthodontic Insurance Benefits

- Financial Planning And Alternative Options If Insurance Falls Short

- Explore Expert Orthodontic Care In Langley With Glow Orthodontics

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Provincial coverage gap | BC’s Medical Services Plan does not cover braces; private dental insurance is your primary option. |

| Age and medical criteria | Most plans cover children aged 7 to 18 for medically necessary orthodontic treatment only. |

| Policy restrictions matter | Waiting periods of 6 to 12 months and lifetime maximums of CAD 1,500 to CAD 3,500 affect affordability. |

| Compare plans carefully | Orthodontic riders, premiums, and coverage limits vary significantly across dental insurance plans. |

| Maximize benefits strategically | Understanding policy details, pre-authorization requirements, and timing optimizes your coverage. |

Understanding orthodontic coverage in Canadian health insurance

BC’s Medical Services Plan (MSP) excludes orthodontic treatments like braces entirely. Private dental insurance is the main source of orthodontic coverage since BC’s MSP excludes braces. This leaves families relying on employer group plans or individual dental policies to manage treatment costs.

Understanding your insurance type is the first step before seeking orthodontic care. Many parents confuse medical and dental insurance, leading to frustrating surprises when filing claims. Private plans may offer orthodontic coverage as optional riders rather than standard benefits.

Verifying specifics with your insurer before starting treatment prevents unwelcome financial shocks. Here’s what you need to know:

- Provincial health plans in BC do not include orthodontic benefits

- Private dental insurance provides the primary coverage pathway

- Orthodontic riders often require additional premiums beyond basic dental coverage

- Coverage details vary widely between insurers and plan types

- Direct communication with your insurance provider clarifies what’s actually covered

Exploring braces insurance coverage in Langley helps you understand local options and requirements specific to BC families.

Age eligibility and medical necessity for orthodontic coverage

Common age limits for orthodontic coverage range from 7 to 18 years. Insurers design these restrictions based on developmental stages when orthodontic intervention proves most effective. Coverage outside this range is rare, even for medically necessary cases.

Medical necessity determines whether your child’s treatment qualifies for reimbursement. Cosmetic improvements alone won’t meet insurer criteria. Documentation from dental specialists proving functional or health impacts is essential for claim approval.

Timing treatments strategically within eligibility windows maximizes your benefits. Starting treatment at age 17 might limit coverage duration compared to beginning at age 10. Parents should coordinate closely with insurers and orthodontists to optimize timing.

Key eligibility factors include:

- Age restrictions typically spanning childhood through late adolescence

- Medical necessity documentation from qualified dental professionals

- Severity assessments measuring functional impairment, not just aesthetics

- Pre-authorization requirements before treatment begins

- Coordination between dental providers and insurance companies

Pro Tip: Schedule a consultation with your orthodontist before your child’s 18th birthday to maximize coverage eligibility, especially if treatment might extend into adulthood.

Understanding orthodontic coverage eligibility helps you plan treatment timing that aligns with policy requirements.

Common exclusions, waiting periods, and policy limits

Waiting periods typically last from 6 to 12 months before coverage activates. This delay means you can’t purchase insurance and immediately file claims for braces. Planning ahead is essential for families anticipating orthodontic needs.

Lifetime maximum orthodontic benefits usually range from CAD 1,500 to CAD 3,500. Once you exhaust this limit, you’re responsible for all remaining costs. Treatment often exceeds these caps, requiring families to budget for significant out-of-pocket expenses.

Cosmetic braces and treatments are commonly excluded from coverage. Insurers distinguish between medically necessary corrections and aesthetic improvements. Clear documentation proving functional issues is critical for claim approval.

Deductibles and co-pays add to your financial responsibility. You might pay 20% to 50% of treatment costs even with coverage. Understanding these cost-sharing structures prevents budget surprises.

Common policy restrictions include:

- Mandatory waiting periods delaying benefit access

- Lifetime maximums capping total orthodontic reimbursement

- Cosmetic treatment exclusions limiting coverage to medical necessity

- Annual benefit limits restricting yearly claim amounts

- Deductibles and co-insurance percentages increasing out-of-pocket costs

Awareness of orthodontic policy limits in BC helps you plan financially and avoid unexpected expenses when treatment begins.

Researching dental insurance waiting periods and exclusions provides detailed policy information specific to British Columbia residents.

Debunking common misconceptions about insurance and braces

Provincial health insurance does not cover braces in BC. Many parents confuse MSP with dental insurance, creating false expectations about coverage. These are entirely separate systems with different benefits and eligibility rules.

Orthodontic coverage is often optional and requires pre-authorization and detailed claim submissions. It’s not automatically included in basic dental plans. You typically need to purchase additional orthodontic riders, which increase your monthly premiums.

Pre-authorization from insurers is commonly required before treatment starts. Skipping this step can result in complete claim denial, leaving you with the full bill. Always confirm approval before your child’s first appointment.

Incomplete or inaccurate claims lead to denials and delays. Missing documentation, incorrect coding, or insufficient medical justification can derail reimbursement. Proper communication between your orthodontist’s office and insurer is critical.

Common misconceptions include:

- Assuming provincial health plans cover orthodontic treatments

- Believing all dental insurance includes orthodontic benefits automatically

- Thinking you can buy insurance after treatment starts and still get coverage

- Expecting full reimbursement without understanding lifetime maximums

- Overlooking pre-authorization and documentation requirements

Pro Tip: Request a pre-determination of benefits from your insurer before treatment. This written estimate shows exactly what they’ll cover, eliminating guesswork about out-of-pocket costs.

Learning about understanding orthodontic insurance coverage clarifies what your policy actually pays for versus common assumptions.

Comparing dental insurance plans for orthodontic benefits in BC

Dental plans differ widely in coverage, premiums, and orthodontic riders. Orthodontic lifetime maximums vary from CAD 1,500 to CAD 3,500; premiums differ by 10-30%. These variations create significant cost differences for families over the treatment period.

Higher lifetime maximums reduce your out-of-pocket expenses but typically require higher monthly premiums. Shorter waiting periods provide faster access to benefits but may cost more upfront. Balancing these factors depends on your financial situation and treatment timeline.

Orthodontic riders often require additional premiums beyond basic dental coverage. Some plans include orthodontic benefits in premium tiers, while others offer them as separate add-ons. Understanding this structure helps you evaluate true monthly costs.

| Plan Feature | Budget Plan | Standard Plan | Premium Plan |

|---|---|---|---|

| Orthodontic Maximum | CAD 1,500 | CAD 2,500 | CAD 3,500 |

| Waiting Period | 12 months | 9 months | 6 months |

| Monthly Premium | CAD 65 | CAD 95 | CAD 125 |

| Orthodontic Rider Cost | CAD 15 | Included | Included |

| Annual Coverage Cap | CAD 750 | CAD 1,250 | CAD 1,750 |

Parents should compare plans using realistic treatment scenarios. If braces cost CAD 5,000 and your plan covers CAD 2,500, you’ll pay CAD 2,500 out of pocket. Factor in waiting periods, deductibles, and co-insurance to calculate total costs accurately.

Key comparison criteria include:

- Lifetime orthodontic maximums and their impact on total coverage

- Waiting period duration before benefits become active

- Monthly premium costs including orthodontic riders

- Annual benefit limits restricting yearly reimbursement

- Co-insurance percentages determining your cost share

Exploring how to compare dental insurance plans BC provides frameworks for evaluating options side by side.

Reviewing British Columbia dental plans comparison resources helps you understand provincial options and regulations.

Practical steps to maximize your orthodontic insurance benefits

Review insurance coverage with providers before starting treatment. Confirm coverage before treatment; submit detailed claims promptly to maximize benefits. This verification prevents misunderstandings about what’s covered and reduces claim denials.

Understand and plan around waiting periods to avoid denied claims. If your policy requires a 12-month wait, purchasing insurance today means coverage starts in 2027. Time enrollment strategically to align with anticipated treatment needs.

Gather and submit complete documentation for claims promptly. Your orthodontist’s office typically handles claim submission, but you should verify they have accurate insurance information. Missing details delay reimbursement or trigger denials.

Follow these steps for maximum benefits:

- Contact your insurer to verify orthodontic coverage details and requirements

- Obtain pre-authorization before scheduling your child’s first orthodontic appointment

- Confirm your orthodontist is in-network to maximize reimbursement rates

- Request a written pre-determination of benefits showing expected coverage amounts

- Track claim submissions and follow up on pending reimbursements promptly

- Keep copies of all documentation, including treatment plans and receipts

- Coordinate payment timing with annual benefit limits to optimize yearly coverage

Pro Tip: If treatment spans multiple calendar years, time major procedures to maximize annual benefit limits. Filing claims in January versus December can double your available coverage for treatments exceeding yearly caps.

Learning how to prepare for braces insurance provides practical guidance on documentation and communication with providers.

Financial planning and alternative options if insurance falls short

Review case studies of families selecting plans covering their needs successfully. Many Langley parents combine employer group coverage with Health Spending Accounts (HSAs) to allocate pre-tax funds for orthodontic expenses. This strategy reduces taxable income while covering gaps in insurance.

Orthodontist payment plans help spread out costs when insurance is limited. Many practices offer interest-free monthly installments over the treatment period. This approach makes braces affordable even with modest insurance coverage.

Explore combining insurance benefits with savings and payment options for comprehensive financial planning. If insurance covers CAD 2,500 and treatment costs CAD 5,000, a 24-month payment plan means roughly CAD 100 monthly for the remaining balance.

Early financial planning reduces stress and helps manage out-of-pocket costs effectively. Starting a dedicated savings account when your child is young gives you years to accumulate funds before treatment begins.

Alternative financing strategies include:

- Health Spending Accounts for pre-tax orthodontic expense allocation

- Orthodontist payment plans with flexible monthly installments

- Medical expense tax credits reducing your annual tax burden

- Flexible Spending Accounts through employer benefit programs

- Personal savings accounts dedicated to anticipated orthodontic costs

Exploring orthodontic financial alternatives provides additional resources for managing treatment costs beyond insurance coverage.

Explore expert orthodontic care in Langley with Glow Orthodontics

Navigating insurance coverage feels overwhelming, but you don’t have to figure it out alone. Glow Orthodontics offers specialized care tailored for Langley families, with resources explaining insurance coverage and treatment options like Invisalign and traditional braces.

Our team helps you understand your specific policy benefits and optimize coverage for your child’s treatment. Parents can access personalized consultations clarifying insurance details, treatment timelines, and financial planning strategies. We work directly with insurers to handle pre-authorizations and claims, reducing your administrative burden.

Whether you’re exploring orthodontic care family guide resources or researching dental insurance covering Invisalign, our experienced team provides answers. Visit Glow Orthodontics to start your child’s confident smile journey with expert guidance and compassionate care.

Frequently asked questions

Does British Columbia’s MSP cover braces for children?

No, BC’s Medical Services Plan does not cover orthodontic treatments like braces. Coverage is primarily through private dental insurance plans purchased individually or obtained through employer group benefits.

What age range is typically eligible for orthodontic insurance coverage?

Most insurance plans cover children aged 7 to 18 years for braces, often requiring medical necessity confirmation from dental specialists. Coverage outside this age range is uncommon even for medically necessary treatments.

How long are waiting periods before orthodontic benefits start?

Waiting periods usually range from 6 to 12 months before orthodontic coverage activates. You cannot purchase insurance and immediately file claims, so plan enrollment well before anticipated treatment needs.

Can cosmetic braces be covered by insurance?

Most plans exclude cosmetic braces from coverage; only medically necessary orthodontic treatments are typically reimbursed. Insurers require documentation proving functional impairment or health impacts, not just aesthetic improvements.

What steps should I take to ensure my orthodontic claim is approved?

Confirm coverage with your insurer before treatment, obtain pre-authorization as required, and submit complete documentation promptly. Request a pre-determination of benefits showing expected coverage amounts to avoid surprises and denials.