Insurance For Orthodontics: Unlocking Braces Coverage

February 27, 2026

Insurance For Orthodontics: Unlocking Braces Coverage

Every parent faces that moment when the dentist says their child might need braces or Invisalign. The search for affordable orthodontic insurance in Langley, British Columbia, can leave families feeling overwhelmed by confusing coverage details and strict age limits. Knowing that insurance often pays only up to 50 percent of orthodontic treatment costs gives you a head start. This guide untangles policy fine print so you avoid costly surprises and confidently plan for your child’s healthiest smile.

Table of Contents

- What Orthodontic Insurance Actually Covers

- Coverage Differences By Plan Type

- Common Limitations You’ll Encounter

- What This Means For Your Family

- Differences Between Braces And Invisalign Coverage

- Why Insurance Favors Traditional Braces

- Coverage Scenarios You’ll Encounter

- Cost Impact On Your Treatment

- How To Verify Your Coverage

- Making Your Decision

- Eligibility, Waiting Periods, And Claim Processes

- Age Restrictions And Eligibility

- The Waiting Period Reality

- Key Eligibility Factors

- The Claims Process Explained

- What Documentation You’ll Need

- Payment During Waiting Periods

- Financial Impact: Out-Of-Pocket Costs And Limits

- Understanding Lifetime Maximums

- Real-World Cost Breakdown

- How Lifetime Maximums Work

- Calculating Your Actual Cost

- Managing Out-Of-Pocket Expenses

- When Costs Exceed Coverage

- Avoiding Common Pitfalls With Orthodontic Insurance

- Pitfall 1: Misunderstanding What’s Actually Covered

- Pitfall 2: Ignoring Retainer Coverage Gaps

- Common Claim Denial Mistakes

- The Medical Necessity Trap

- Deadline And Timing Issues

- Network Provider Mistakes

- Lifetime Maximum Misunderstandings

Key Takeaways

| Point | Details |

|---|---|

| Orthodontic insurance varies by plan | Coverage for braces and Invisalign can differ, often with braces receiving more support than aligners. |

| Understand your policy limits | Check your policy for lifetime maximums and coverage percentages to avoid unexpected out-of-pocket costs. |

| Be aware of common exclusions | Items like retainers may not be covered; confirm all aspects of your plan before starting treatment. |

| Documentation is crucial | Ensure all required documentation is complete and submitted on time to prevent claims denials. |

What Orthodontic Insurance Actually Covers

Orthodontic insurance doesn’t work the same way as your regular dental coverage. Most standard dental plans simply don’t include braces or Invisalign at all.

When orthodontic coverage does exist, it typically follows these patterns:

- Percentage-based coverage: Insurance pays a portion of treatment costs, commonly up to 50% of orthodontic treatment costs, though some plans cover 25% or 75%

- Lifetime maximum limits: You have a set dollar amount available for orthodontic care over your lifetime, often separate from general dental maximums

- Age-based restrictions: Most policies limit coverage to children and teenagers, with adult coverage being rare

- Medical necessity requirements: Some plans only pay if an orthodontist documents that treatment is medically necessary, not cosmetic

Coverage Differences by Plan Type

Not all orthodontic insurance is created equal. Children’s coverage is significantly more common than adult coverage due to Essential Health Benefit mandates in Canada.

Supplemental orthodontic insurance exists separately from standard dental plans. Many families in Langley add this specific coverage to their existing plans to fill the gap.

Common Limitations You’ll Encounter

Orthdontic plans often include waiting periods before coverage kicks in. You might need to wait 6 to 12 months after enrollment before benefits activate.

Network restrictions are standard. Insurance typically requires you to use an in-network provider, or your coverage percentage drops significantly.

Age limits create real problems for adult patients. Most plans cover only patients under age 19, though some policies extend to age 26.

Preexisting conditions may not be covered. Treatment already started before your policy begins is usually excluded.

Below is a quick summary of common orthodontic insurance limitations and their impact:

| Limitation | What It Means for Patients | Typical Result |

|---|---|---|

| Waiting period | Must wait months after enrolling | Delays treatment start |

| Age restrictions | Adults often ineligible | Limits coverage to youth |

| Network requirements | Must use specific providers | Reduced coverage out-of-network |

| Preexisting treatment rules | Coverage not valid for ongoing care | Costs not reimbursed |

Most dental plans don’t include orthodontics by default, but supplemental insurance can add this coverage for families seeking comprehensive protection.

What This Means for Your Family

If your current plan covers orthodontics, check your policy documents for exact percentages and lifetime limits. Those numbers directly impact your out-of-pocket costs.

If your plan doesn’t cover orthodontics, supplemental insurance or paying out-of-pocket become your options. Many families use payment plans to spread costs over treatment duration.

Understanding your specific coverage prevents sticker shock when treatment quotes arrive. Ask your plan provider for written clarification about your exact benefits before starting treatment.

Pro tip: Request your insurance company’s written explanation of orthodontic benefits before your initial consultation, so we at Glow Orthodontics can provide accurate cost estimates and help you maximize your coverage.

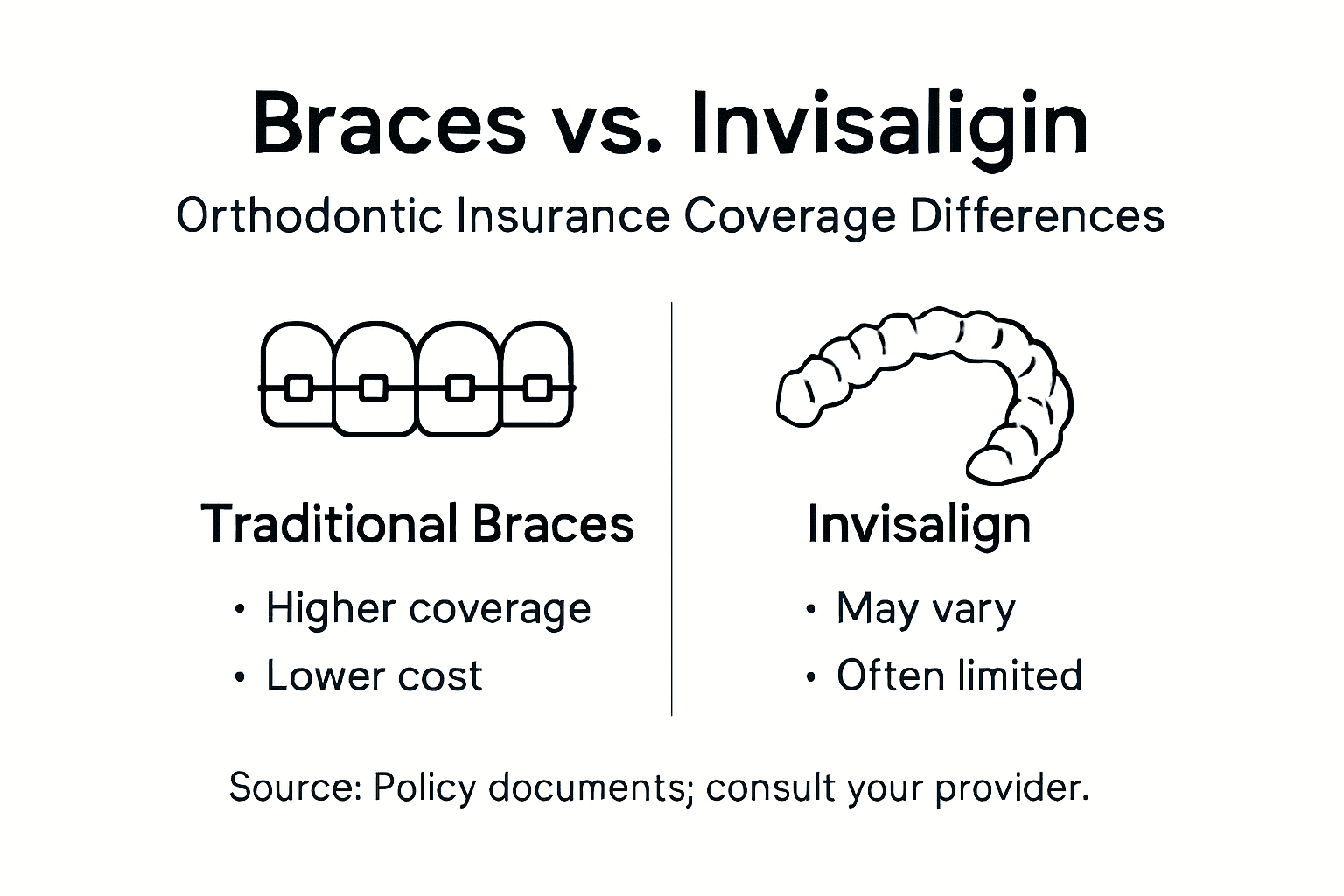

Differences Between Braces And Invisalign Coverage

Insurance companies treat braces and Invisalign differently, and that difference hits your wallet hard. Understanding the coverage gap between these two options helps you plan your budget before treatment starts.

Why Insurance Favors Traditional Braces

Traditional metal braces are the gold standard for insurance coverage. Most plans cover them at higher percentages because they’re fixed appliances with decades of proven success.

Invisalign aligners occupy a gray area. Insurance coverage often depends on medical necessity and severity of your orthodontic issue, meaning some plans cover them fully while others don’t cover them at all.

Coverage Scenarios You’ll Encounter

Different plans handle Invisalign in three main ways:

- Fully covered: Treated the same as braces with identical percentage payouts and lifetime maximums

- Partially covered: Lower percentage coverage than traditional braces, sometimes 25% instead of 50%

- Not covered: Explicitly excluded from orthodontic benefits, requiring out-of-pocket payment

Some insurance policies explicitly state whether Invisalign is included or excluded. Others remain vague, forcing you to call and ask directly.

Cost Impact on Your Treatment

Braces typically cost $3,000 to $7,000 in the Langley area. If insurance covers 50%, you pay $1,500 to $3,500.

Invisalign generally costs $4,000 to $9,000. If your plan covers it at only 25%, your out-of-pocket jumps significantly compared to braces coverage.

Here’s how coverage for braces and Invisalign typically differs:

| Factor | Braces Coverage | Invisalign Coverage |

|---|---|---|

| Insurance approval | Standard, widely accepted | Often varies, sometimes excluded |

| Out-of-pocket impact | Usually lower due to higher coverage | Often higher, especially if only partial coverage |

| Lifetime max effects | Reaches maximum more slowly | Reaches maximum quickly at higher costs |

| Medical necessity | Rarely required | Often required for reimbursement |

Insurance coverage tends to favor traditional braces for severe cases, whereas clear aligners suit many orthodontic problems, making plan type the deciding factor for many families.

How to Verify Your Coverage

Call your insurance company and ask these specific questions:

- Does your plan cover Invisalign at all?

- If yes, what percentage does it cover?

- Are there different limits for braces versus Invisalign?

- Does medical necessity affect Invisalign coverage?

Get written answers. Email confirmations protect you from coverage surprises later.

Making Your Decision

If your plan covers both equally, Invisalign may be worth the slightly higher treatment cost for lifestyle convenience. If your plan covers braces but not Invisalign, braces become the financially smart choice.

Some families choose Invisalign anyway and pay the difference out-of-pocket. Others prioritize what insurance covers to minimize costs.

Pro tip: Bring your insurance policy information to your consultation so Glow Orthodontics can calculate exact out-of-pocket costs for both braces and Invisalign options tailored to your specific coverage.

Eligibility, Waiting Periods, And Claim Processes

Not everyone qualifies for orthodontic insurance benefits immediately, and the path to getting covered involves several steps. Understanding these rules upfront prevents frustration when you’re ready to start treatment.

Age Restrictions And Eligibility

Most orthodontic insurance plans limit coverage to dependents under age 18 or 19. Adult coverage exists but remains rare and typically requires higher-tier policies or supplemental insurance.

If you’re an adult seeking coverage, check whether your employer offers enhanced dental plans. Some companies in British Columbia include adult orthodontic benefits as part of premium health packages.

Age eligibility also depends on when you enroll. Plans calculate age limits from enrollment date, so timing matters if your child is approaching the cutoff.

The Waiting Period Reality

Most plans impose waiting periods from 6 to 12 months before orthodontic coverage activates. This means you can’t start treatment immediately after getting insurance.

Waiting periods prevent people from enrolling, getting expensive work done, then dropping coverage. Insurance companies use them to avoid short-term enrollment abuse.

Some plans waive waiting periods for group coverage through employers. Check your policy documents to see if yours does.

Key Eligibility Factors

Beyond age, these requirements affect your eligibility:

- Active coverage: You must maintain continuous insurance; lapses reset waiting periods

- Preexisting conditions: Treatment started before enrollment typically doesn’t qualify

- Network requirements: In-network providers maximize your benefits; out-of-network reduces coverage

- Medical necessity documentation: Some plans require your orthodontist to justify treatment medically

The Claims Process Explained

Submitting claims requires specific documentation. Claim processes include ensuring treatment by in-network providers and submitting proper documentation for reimbursement.

Your orthodontist typically handles this automatically. You sign authorization forms, and Glow Orthodontics submits claims directly to your insurance company.

For out-of-network treatment, you’ll submit claims yourself using receipts and itemized invoices your orthodontist provides.

What Documentation You’ll Need

Have these items ready when starting treatment:

- Insurance policy number and group number

- Confirmation of waiting period expiration date

- Orthodontist’s pre-treatment authorization from insurance

- Itemized treatment plan and cost breakdown

- Dental claim forms your orthodontist requests

Missing documentation delays claims and payment reimbursement.

Age limits and waiting periods are the biggest barriers to coverage, so planning around these timelines maximizes your insurance benefits.

Payment During Waiting Periods

You can start treatment immediately, but you’ll pay full price until the waiting period ends. Many families use payment plans to spread costs during this time.

Flexible spending accounts through your employer can offset out-of-pocket costs if you have them available.

Pro tip: Contact your insurance company at least two months before your planned treatment start to confirm your waiting period end date and required documentation, then bring this confirmation to your Glow Orthodontics consultation.

Financial Impact: Out-Of-Pocket Costs And Limits

Even with insurance, orthodontic treatment requires significant out-of-pocket spending. Knowing your financial limits upfront helps you budget and avoid surprise bills.

Understanding Lifetime Maximums

Most orthodontic plans include a lifetime maximum, typically ranging from $1,200 to $2,000 per person. This is the total amount your insurance will ever pay for orthodontic care.

Treatment costs often exceed these limits significantly. Insurance usually covers about 50% of costs up to a lifetime maximum, meaning you pay the remainder out-of-pocket.

If your plan covers 50% but treatment costs $6,000, and your lifetime maximum is $1,500, insurance pays only $1,500. You’re responsible for the other $4,500.

Real-World Cost Breakdown

Let’s look at typical costs for families in Langley:

- Total braces treatment: $4,500 to $7,500

- Insurance coverage at 50%: $2,250 to $3,750

- Your out-of-pocket share: $2,250 to $4,500 (plus anything exceeding lifetime max)

Invisalign typically runs higher at $5,000 to $9,000, pushing out-of-pocket costs even further.

How Lifetime Maximums Work

Your lifetime maximum doesn’t reset yearly like general dental benefits. You have one total amount for your entire life with that insurance company.

If you’ve previously used part of your maximum for braces as a child, less remains available for future orthodontic needs.

Changing insurance companies gives you a fresh lifetime maximum with the new provider.

Calculating Your Actual Cost

Use this formula to estimate your out-of-pocket expense:

- Get treatment cost estimate from your orthodontist

- Multiply by your plan’s coverage percentage (typically 50%)

- Cap at your lifetime maximum if needed

- Subtract that from total cost

- That’s your out-of-pocket responsibility

Example: $6,000 treatment × 50% = $3,000 insurance pays (if under lifetime max). You pay $3,000.

Most families underestimate their out-of-pocket costs because they forget insurance pays only up to lifetime maximums, not percentages indefinitely.

Managing Out-Of-Pocket Expenses

Several strategies help reduce your financial burden:

- Payment plans: Glow Orthodontics offers flexible payment schedules spreading costs over treatment duration

- Flexible spending accounts: Use pre-tax dollars through your employer if available

- Health savings accounts: Similar to FSAs, these provide tax-advantaged savings

- Employer reimbursement: Some companies reimburse orthodontic costs; check your benefits

When Costs Exceed Coverage

If treatment exceeds your lifetime maximum, you’ll pay the difference directly. This is common and expected for comprehensive cases.

Ask your orthodontist for itemized estimates separating essential versus elective components. Sometimes you can adjust treatment scope to fit budget constraints.

Pro tip: Request a detailed cost estimate and have Glow Orthodontics verify your exact insurance coverage amount before treatment begins, so you know your precise out-of-pocket responsibility and can arrange payment plans accordingly.

Avoiding Common Pitfalls With Orthodontic Insurance

Many families leave money on the table by making preventable insurance mistakes. Knowing these common errors helps you protect your benefits and avoid frustrating claim denials.

Pitfall 1: Misunderstanding What’s Actually Covered

Families often assume their plan covers everything orthodontic. Read your policy carefully because coverage varies dramatically between plans.

Some plans exclude Invisalign entirely. Others cover braces but not retainers, or require higher copays for certain appliances. Don’t assume; verify every detail.

Pitfall 2: Ignoring Retainer Coverage Gaps

Here’s the surprise many families face: A frequent pitfall is misunderstanding coverage for post-treatment retainers, which some insurance plans exclude entirely or classify differently from active treatment.

You might finish braces with full insurance support, then discover retainers cost $1,500 out-of-pocket. Ask about retainer coverage before treatment starts.

Retainers are essential and permanent. Your child will need them for life. Budget accordingly.

Common Claim Denial Mistakes

These errors trigger denied claims more than anything else:

- Incomplete documentation: Missing forms, unsigned authorizations, or incomplete treatment plans

- Incorrect billing codes: Typos or wrong procedure codes on claims

- Medical necessity issues: Failing to document why treatment is medically necessary, not cosmetic

- Network provider violations: Using out-of-network providers without authorization

- Timing problems: Submitting claims after deadlines or before waiting periods end

The Medical Necessity Trap

Some insurance plans require documentation that treatment is medically necessary, not cosmetic. Severe crowding or bite issues qualify, but mild misalignment might not.

Ask your orthodontist whether they’ll document medical necessity for your case. If your plan requires it and your orthodontist can’t provide it, coverage may be denied.

Ensuring thorough documentation and accurate coding is critical to avoid claim issues, so review all paperwork before submission.

Deadline And Timing Issues

Insurance companies have strict claim submission deadlines, often within 30 to 90 days of treatment completion. Glow Orthodontics handles this, but verify they’ve submitted claims.

Waiting periods must also expire before claims process. If your waiting period ends in March, don’t expect coverage for treatment started in February.

Network Provider Mistakes

Using out-of-network providers without explicit pre-authorization is expensive. Your coverage percentage drops, sometimes to zero.

Verify Glow Orthodontics is in-network with your insurance before committing. Out-of-network treatment rarely gets reimbursed at acceptable rates.

Lifetime Maximum Misunderstandings

Many families forget lifetime maximums don’t reset yearly. They think they get $1,500 annually, then face surprise denials when claims exceed the lifetime cap.

Calculate your remaining benefits early. If you’ve used $800 of a $1,500 lifetime maximum, only $700 remains for future orthodontic care.

Pro tip: Request written confirmation from your insurance company listing your exact lifetime maximum, coverage percentage, waiting period status, and retainer coverage before your consultation so Glow Orthodontics can provide accurate cost estimates.

Unlock Your Smile Potential With Expert Orthodontic Insurance Guidance

Navigating orthodontic insurance can feel overwhelming with waiting periods, lifetime maximums, and varied coverage between braces and Invisalign. At Glow Orthodontics, we understand these challenges and offer personalized solutions that help you maximize your insurance benefits while creating the perfect treatment plan for your family’s needs. From verifying your exact coverage details to explaining out-of-pocket costs clearly, our warm and professional team is here to guide you every step of the way.

Don’t let confusion about insurance hold you back from achieving a confident smile. Take the first step today by scheduling a consultation with Glow Orthodontics to receive a tailored insurance review and transparent cost estimate. Visit Glow Orthodontics to learn more about our services and book your appointment online with ease. Your path to a glowing smile starts here.

Frequently Asked Questions

What does orthodontic insurance typically cover?

Orthodontic insurance usually covers a percentage of treatment costs, often up to 50%, but can vary between 25% to 75%. It may also have lifetime maximum limits that separate it from general dental coverage.

Are there age restrictions for orthodontic insurance coverage?

Yes, most policies limit coverage to children and teenagers, often capping it at ages 18 or 19. Adult coverage is rare and typically requires additional or supplemental insurance plans.

How do braces and Invisalign coverage differ under insurance?

Insurance generally favors traditional metal braces, often covering them at higher percentages. Invisalign coverage can vary significantly; some plans may fully cover, partially cover, or exclude them altogether based on medical necessity.

What should I do if my treatment exceeds my orthodontic insurance limits?

If your treatment costs exceed your insurance’s lifetime maximum, you’ll need to pay the difference out-of-pocket. It’s wise to ask for a detailed cost estimate before starting treatment to plan for any potential additional expenses.